The centre of gravity in global automotive research and product development is continuing to shift eastward. Chinese carmakers, once viewed as followers in the global industry, are increasingly exporting technology and expertise back to established international giants. A new industrial path — one defined by “Chinese technology feeding global innovation” — is rapidly taking shape.

Recently, Cui Dongshu, secretary-general of the China Passenger Car Association, noted that “the global centre of automotive production and sales continues to move towards East Asia, fundamentally reshaping the global automotive supply chain.” That observation is being reinforced by nearly every new development emerging from China’s car market today.

The 2026 Beijing Auto Show has just concluded, with dozens of major new models unveiled. Yet what truly caught the industry’s attention was not only the vehicles themselves, but the posture adopted by Germany’s traditional luxury trio — BMW, Mercedes-Benz and Audi — which appeared increasingly willing to set aside the long-held prestige of “German engineering” in favour of deeper compromises with Chinese technology and market realities.

Roughly 70 per cent of the software code behind BMW’s Neue Klasse system is now developed by Chinese teams. Audi has deepened cooperation with Huawei on intelligent driving systems. Mercedes-Benz’s Chinese research teams are taking leading roles in smart vehicle development. Across the board, the research focus and product decision-making power of Germany’s luxury brands are shifting steadily towards China.

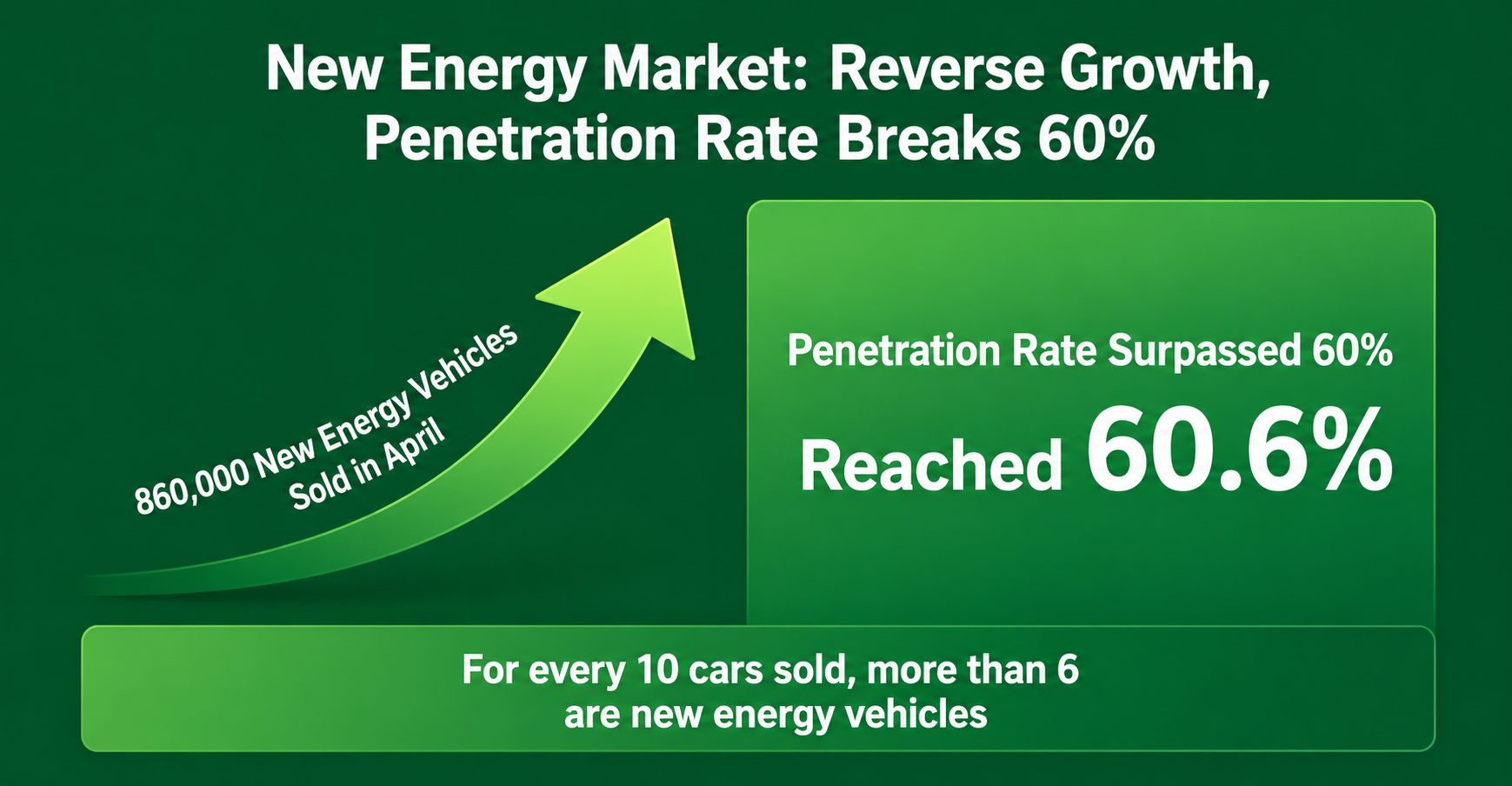

This strategic transition mirrors broader market trends. Data from April showed China’s new-energy vehicle penetration rate surpassing 60.6 per cent for the first time, while domestic brands claimed more than 65 per cent of the passenger-car market. Joint-venture brands, once dominant, have now fallen below a 20 per cent share. The decades-old model of “trading market access for foreign technology” has been fundamentally rewritten.

BBA’s China Strategy Enters a New Phase

During the first quarter of 2026, the moves made by BMW, Mercedes-Benz and Audi became impossible to ignore. Although each company has chosen a different path, the message is increasingly clear: whoever fully understands the Chinese market may define the next era of luxury automobiles.

Audi has moved earliest — and most aggressively — in embracing localisation. On April 17, Audi and SAIC Motor signed an expanded strategic cooperation agreement to establish the Audi Innovation Technology Centre in Shanghai. Led by Audi but jointly developed by Chinese and German teams, the centre is highly symbolic. It represents Audi’s first “full-value-chain” research entity outside Europe and reflects ambitions that go beyond China itself.

Based on the next-generation Advanced Digitised Platform (ADP), the two sides are jointly developing four new AUDI-branded models. The first SUV model, the E7X, began pre-sales on May 8 and has been positioned as a “smart performance flagship SUV”. It is also expected to become Audi’s first global model capable of delivering Level 3 autonomous driving.

According to company plans, Audi’s two brands in China will launch six pure-electric vehicles by the end of 2026. Gernot Döllner, chairman of Audi’s management board, described the upgraded cooperation and the new technology centre as a critical step in strengthening Audi’s long-term position in China and responding more effectively to rapidly evolving consumer demand.

Mercedes-Benz, by contrast, appears to have fallen behind its rivals. While Audi prioritised local research capabilities, Mercedes has opted for deeper technological dependence. Industry sources suggest Mercedes has reached an agreement with Geely to adopt the latter’s GEEA 4.0 electronic and electrical architecture for a new electric platform codenamed “Phoenix”.

The cooperation marks the first time the two companies have moved beyond powertrain collaboration into full vehicle-level technological integration. Yet the move also highlights a difficult reality for Mercedes: in critical underlying architecture, the company increasingly needs Chinese technological support.

The “Phoenix” platform is expected to underpin a range of entry-level global electric vehicles, including the A-Class, B-Class, GLA, GLB and CLA, with mass production targeted for 2030. Mercedes-Benz’s China R&D centre has already been upgraded into the company’s global compact-car development headquarters, while Geely’s earlier GEEA 3.0 platform has already supported vehicle sales exceeding one million units.

In intelligent driving and battery technologies, Mercedes continues to deepen cooperation with Chinese autonomous driving company Momenta. Reports also suggest the German carmaker is in talks with BYD regarding battery supply partnerships. While these moves demonstrate urgency, they also underline Mercedes’ increasingly reactive position in key electric and smart-vehicle technologies.

BMW, meanwhile, is attempting to accelerate its catch-up efforts through Spotlight Automotive, its joint venture with Great Wall Motor. On March 31, BMW board member Frank Weber, who oversees research and development, visited Great Wall Motor to discuss deeper technical cooperation and progress on the Spotlight project.

Since the launch of the electric MINI, Spotlight Automotive has delivered relatively strong results. In June 2025, the company rolled out its 100,000th electric MINI vehicle. During the 2026 Beijing Auto Show, MINI senior vice-president Jean-Philippe Parain stated that one-third of MINI’s total sales in 2025 came from electric vehicles and praised cooperation with Spotlight Automotive.

More importantly, Spotlight Automotive has become not only MINI’s global export hub, but also a testing ground for a broader “Made in China, Sold Globally” strategy. Electric MINI models produced in China are already being exported to Germany, Britain, France, Japan and Thailand among other markets. Whether BMW can regain momentum in 2026 may prove to be one of the company’s greatest tests in years.

Forced to Abandon Old Assumptions

Behind the collective strategic pivot of Germany’s luxury brands lies mounting commercial pressure.

The Chinese market has changed dramatically. In the first quarter of 2026, domestic passenger-car brands sold 2.862 million vehicles, pushing market share to a record 67.9 per cent. Joint-venture brands, meanwhile, fell to just 24.9 per cent, down sharply from 45.6 per cent in 2021.

Data from the China Passenger Car Association showed that new-energy vehicle penetration exceeded 60 per cent in April, while domestic brands have effectively broken through in the premium segment above RMB200,000.

The pure-electric sales performance of BBA has been particularly alarming. Statistics suggest that in 2025, the combined pure-electric sales of BMW, Mercedes-Benz and Audi in China remained below 300,000 units. By comparison, newer brands such as NIO, Li Auto, Xiaomi and Tesla each recorded annual sales exceeding 200,000 vehicles individually.

Mercedes-Benz’s early electric products struggled especially badly. Combined sales of the EQB, EQE SUV and EQA models between January and July 2025 totalled fewer than 5,000 vehicles. Pure-electric models accounted for less than 2 per cent of Mercedes’ overall China sales.

Technological weaknesses have also become increasingly difficult to ignore. Mercedes-Benz’s early EQC model was built on a modified combustion-engine platform, resulting in limited range and underwhelming in-car experience. BMW’s iX3 and i3 models were criticised for insufficient localisation and poor adaptation of intelligent driving functions. Audi, meanwhile, moved too slowly, missing market opportunities as production of vehicles based on its PPE platform was repeatedly delayed.

At the same time, the traditional fuel-powered vehicle market has been shrinking rapidly. As Chinese brands continue to break into the premium segment, competition in luxury electric vehicles has intensified dramatically. Consumers are increasingly prioritising intelligent features, battery range and localised user experience over traditional notions of prestige and brand heritage.

At the beginning of 2026, all three German luxury brands reshuffled senior leadership in China. In essence, these changes reflected strategic self-correction amid failures in electrification and lagging progress in intelligent technologies. And as pricing systems begin to weaken, the once untouchable aura of German luxury has started to bend under the pressure of market reality.

From “Market for Technology” to “Technology for Market”

Within just a few years, Chinese carmakers have transformed themselves from followers into emerging rule-makers.

Under the old “Joint Venture 1.0” model, foreign companies supplied the technology, standards and branding, while Chinese partners focused primarily on manufacturing and market operations. Today, however, Chinese firms are increasingly shaping the direction of the industry through their early lead in electrification and smart technologies.

The deeper significance lies in how the nature of cooperation itself is changing. Technologies developed at Audi’s Shanghai innovation centre are expected to feed back into Audi’s global product line-up, creating a genuine model of “local research, global output”. Mercedes-Benz’s “Phoenix” platform, based on Geely architecture, will support entry-level electric vehicles intended for international markets. Electric MINI vehicles produced by Spotlight Automotive are already being exported to 15 countries, with roughly 80 per cent of output destined for overseas markets.

China is no longer simply a manufacturing base for global luxury cars. Increasingly, it is becoming a core centre for the development and export of next-generation automotive technologies. Backed by first-mover advantages in electrification and intelligent systems, Chinese carmakers are evolving from supporting players within the global supply chain into forces that can no longer be ignored.

For foreign luxury brands, this raises a long-debated question that is now becoming unavoidable: once Chinese companies fully control technological leadership, what remains at the heart of cooperation between Chinese and foreign carmakers? Brand value? Distribution networks? Or perhaps the lingering prestige accumulated over decades?

As the era of electrification and intelligent vehicles accelerates, the ultimate contest facing BMW, Mercedes-Benz and Audi in China may only just be beginning. Whether these brands can stage a successful revival could depend largely on how effectively these new forms of “reverse joint ventures” ultimately perform.