India’s electric-vehicle story is becoming harder to separate from China’s industrial power.

Sales of electric cars and scooters have climbed after Prime Minister Narendra Modi urged Indians to embrace battery-powered vehicles as a way to cut the country’s fuel-import bill. For investors, it has offered the familiar promise of a vast consumer market moving toward electrification. For policymakers, it has exposed a less comfortable reality: many of the materials and technologies behind that transition still run through China.

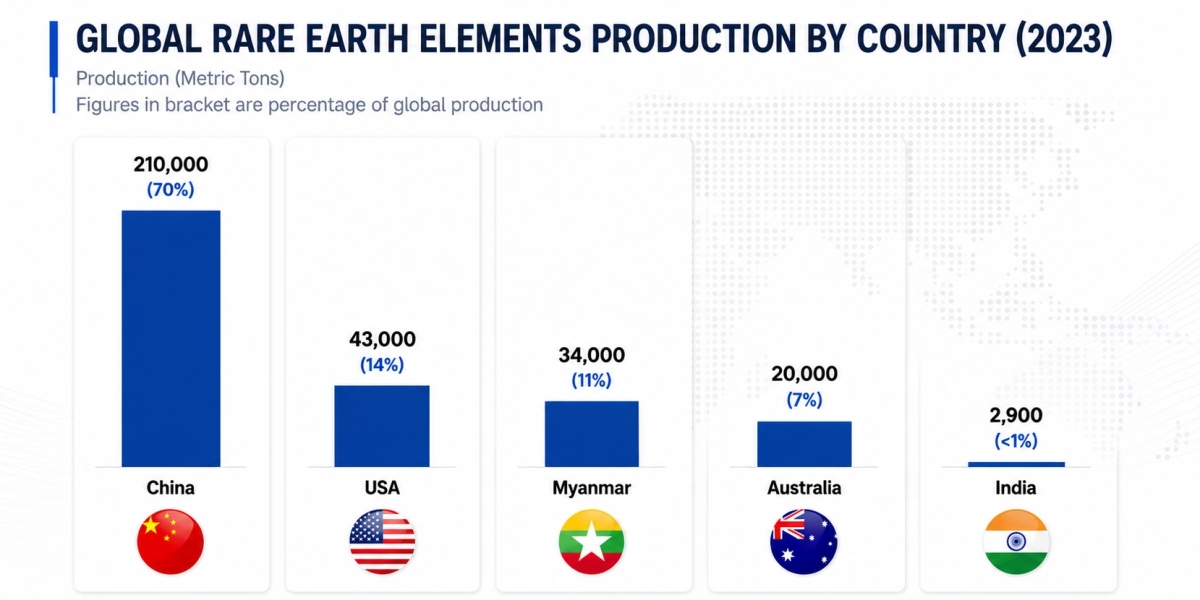

India lacks sufficient access to the critical minerals and processing capabilities needed to manufacture core EV components, from lithium-ion cells to rare-earth permanent magnets. In the 2025-26 fiscal year, India’s lithium-ion battery imports rose 64% to about $4.375 billion, with China accounting for 84% of the total. In rare-earth minerals and magnets, India’s dependence on China is estimated at 85% to 90%.

That reliance has moved from a strategic concern to a production risk. China’s 2025 restrictions on exports of rare-earth permanent magnets hit Indian automakers directly, underlining how vulnerable the country’s EV ambitions remain to decisions made in Beijing.

A Battery Plan That Has Yet to Deliver

New Delhi has tried to build a domestic battery-manufacturing base, but progress has been slow. Its advanced chemistry cell production-linked incentive programme, worth about $1.901 billion, allocated 40GWh of battery-manufacturing capacity and subsidy eligibility to selected companies.

Only a small number of projects have reached commercial operation. Others have been delayed by disputes, weak execution and the complexity of starting a sector in which India has little industrial depth. ACC Energy Storage has faced scrutiny over alleged misrepresentation, traditional lead-acid battery makers were left outside the scheme, and several manufacturers have been held back by delayed equipment deliveries, a shortage of foreign technical specialists and tighter export controls.

The problem is not only that factories are late. It is that factories alone do not create a battery industry. India still lacks the dense supplier networks, trained workforce, process know-how and upstream material ecosystem that allow Chinese producers to operate at scale.

The Cost Gap With China

The economics remain unforgiving. Batteries made in India are estimated to cost 25% to 30% more than those made in China, making it difficult for local producers to compete in a price-sensitive vehicle market.

Upstream weaknesses are even more acute. India has almost no large-scale processing capacity for some essential materials. Graphite supply is almost entirely dependent on China, and a serious disruption would leave Indian companies searching for alternatives that may be either unavailable or prohibitively expensive.

The technology gap is just as important. Lithium iron phosphate batteries, widely seen as well suited to India’s hot climate and cost-conscious market, rely on know-how that remains heavily concentrated in China. Chinese authorities have also become more cautious about allowing companies to transfer battery technology to India, narrowing one of the fastest routes for Indian firms to close the gap.

Subsidies With Too Much Risk Up Front

The design of India’s incentive system has added another constraint. Companies in the ACC-PLI programme must carry much of the execution risk before they can receive support. If a manufacturer runs out of capital before a project qualifies for subsidies, the state support may arrive too late to matter.

That structure has damped investor appetite in a sector that already requires heavy upfront spending. It has also created a chicken-and-egg problem for the broader supply chain. Because battery manufacturing has moved slowly, upstream material producers have limited domestic customers and are increasingly looking to export markets such as the US instead.

Recycling Becomes the Strategic Shortcut

With manufacturing barriers proving difficult to clear, India is turning more attention to battery recycling and overseas mineral assets. Recycling is now viewed by parts of the industry as one of the most practical ways to reduce dependence on China for critical minerals.

Some forecasts suggest recycling could eventually account for 30% to 50% of India’s critical-mineral capacity. Other estimates say recycled materials could meet as much as 60% of India’s cobalt demand, 70% of its lithium carbonate needs and 75% of its rare-earth requirement.

New Delhi is also supporting domestic magnet production through a rare-earth permanent magnet programme worth about $764 million. Several Indian companies are moving into the sector, while the government continues to rely on Indian Rare Earths Ltd as the country’s only state-backed rare-earth magnet producer.

The Overseas Push

India is also trying to secure resources beyond its borders. KABIL, the state-backed overseas mineral acquisition company, has obtained access to five lithium blocks in Argentina, part of a broader push to reduce exposure to Chinese-controlled supply chains.

That effort mirrors the strategy pursued by other industrial powers: diversify mining, build refining capacity, localise parts of the value chain and use recycling to close the loop. The challenge is that China spent decades building its position in critical minerals, from mining and processing to equipment, chemistry and manufacturing scale. India is trying to compress that learning curve into a few years.

India’s EV Boom Meets Its Supply-Chain Reality

The global auto industry is moving toward batteries, magnets and software. For India, the shift offers a chance to build a new industrial base rather than remain an importer of oil and components. Yet the country’s EV boom is still resting on supply chains it does not control.

Breaking China’s grip will require more than subsidies and headline factory announcements. India will need patient capital, processing expertise, reliable access to minerals, a domestic customer base for upstream suppliers and technology partnerships that can withstand geopolitical pressure.

Until then, India’s electric-vehicle ambitions will remain caught between two forces: a fast-growing home market that wants cleaner mobility, and a global battery supply chain still shaped overwhelmingly by China.