Chinese autonomous driving company Momenta has cleared its Hong Kong Stock Exchange listing hearing and is preparing to launch its IPO as early as June 2026, targeting at least $10 billion in proceeds. The implied valuation exceeds $100 billion, according to its prospectus disclosures.

BYD emerges as largest customer as China’s autonomous driving contender heads toward Hong Kong listing

Founded in 2016, Momenta has positioned itself as one of China’s most prominent providers of mass-production assisted driving software, with a dual-track strategy spanning Level 2 driver assistance systems and Robotaxi development.

According to the IPO filing, BYD has become Momenta’s largest customer. The company’s assisted driving business has seen its gross margin rise nearly fourfold over the past two years, underscoring a rapid shift in revenue composition.

From engineering services to licensing: a margin structure transformed

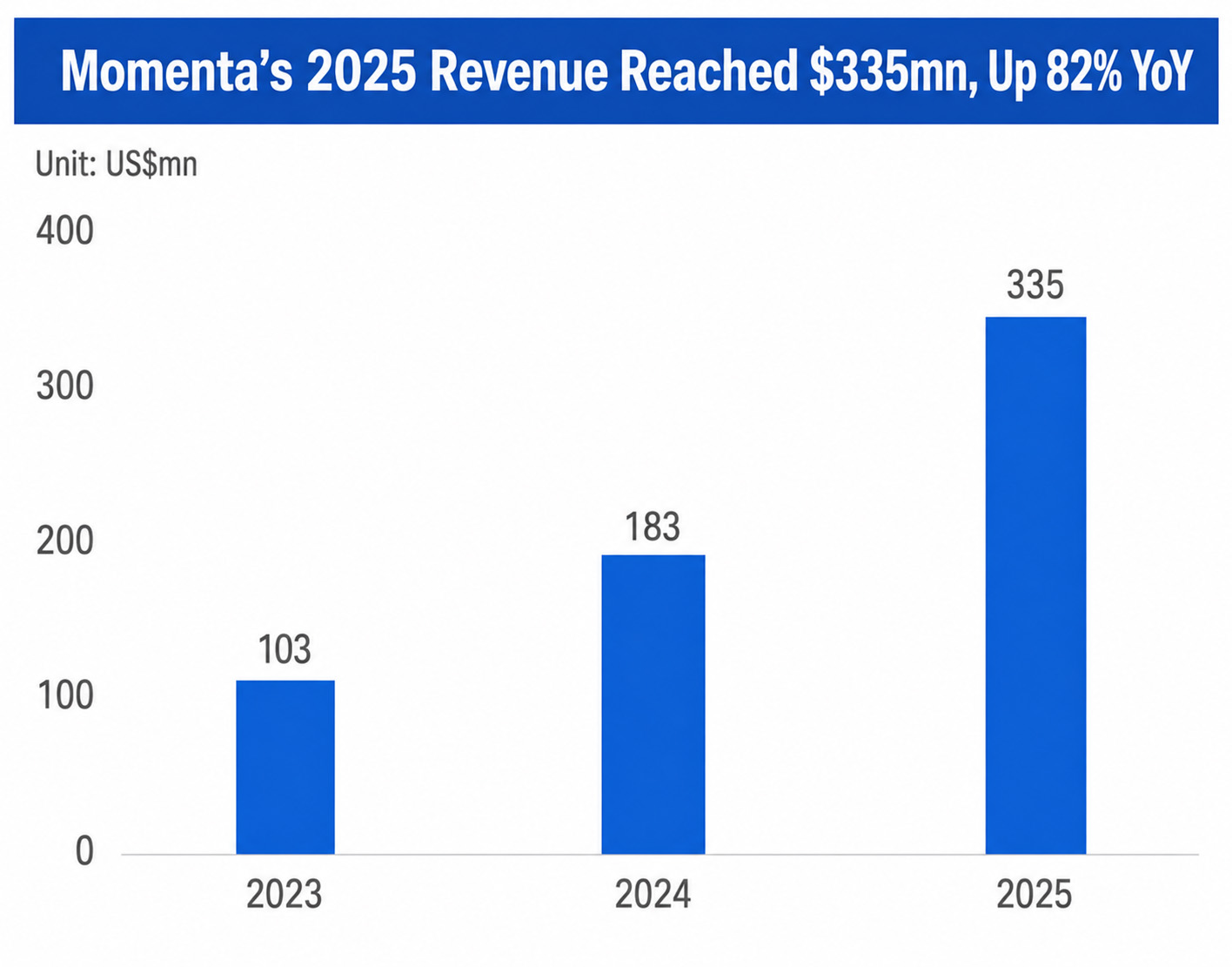

Momenta’s financial profile has shifted sharply toward higher-margin software licensing. Gross margin climbed from 17.5% in 2023 to 71.6% in 2025, a level typically associated with mature software businesses rather than automotive suppliers.

The key driver is a transition away from bespoke engineering services toward per-vehicle licensing fees embedded in mass production models. In 2023, licensing contributed just 3.1% of revenue. By 2025, it accounted for 40.1%.

This model scales with vehicle deliveries rather than one-off project work. That also exposes revenue to cyclicality in auto demand, model replacement risk, and competitive substitution from rival suppliers or in-house systems developed by automakers.

Customer concentration and structural dependency risks

The filing shows a high degree of customer concentration. The top five customers contributed between 62.6% and 86.7% of revenue over the past three years. BYD is estimated to account for 21.6% in 2025, making it the single largest client.

Such concentration increases sensitivity to shifts in procurement strategies among automakers, many of which also act as strategic investors in competing autonomous driving technologies.

Losses narrow on an adjusted basis, but widen underneath

On an adjusted basis, Momenta reports a narrowing loss from 1.09 billion yuan to 300 million yuan, aided by the exclusion of non-cash items such as share-based compensation and fair value changes.

On a statutory basis, the picture is less favorable. Net losses widened from 2.57 billion yuan to 3.46 billion yuan over three years, bringing cumulative losses to approximately 9.2 billion yuan.

That equates to roughly $1,278,000,000 based on standard FX assumptions.

Heavy R&D spending and balance sheet strain

The company continues to invest aggressively in engineering talent and R&D. As of December 2025, Momenta employed 1,157 engineers and technical staff, representing around 80% of its workforce.

R&D expenses rose from 1.28 billion yuan in 2023 to 1.87 billion yuan in 2025, bringing cumulative spending above 5 billion yuan.

Net debt reached 17.89 billion yuan (approximately $2,485,000,000), while current liabilities exceeded assets by more than 19 billion yuan. Cash stood at 1.3 billion yuan at year-end 2025, against negative operating cash flow of 280 million yuan.

Management indicates existing liquidity can support operations for roughly 12 months, with IPO proceeds and preferred share conversions expected to strengthen the balance sheet.

Robotaxi ambitions remain early-stage and capital intensive

Momenta continues to develop its Robotaxi business through partnerships and testing programs, including integration with Uber, trials in Munich and Abu Dhabi, and collaborations with Mercedes-Benz and Lumo.

Despite these efforts, Robotaxi remains a non-material contributor to revenue. The business is currently characterized by net cash outflow and depends on large-scale Level 4 commercialization to achieve profitability.

Regulatory tightening around autonomous ride-hailing permits in China adds another layer of uncertainty to expansion timelines.

Valuation debate: premium pricing versus global peers

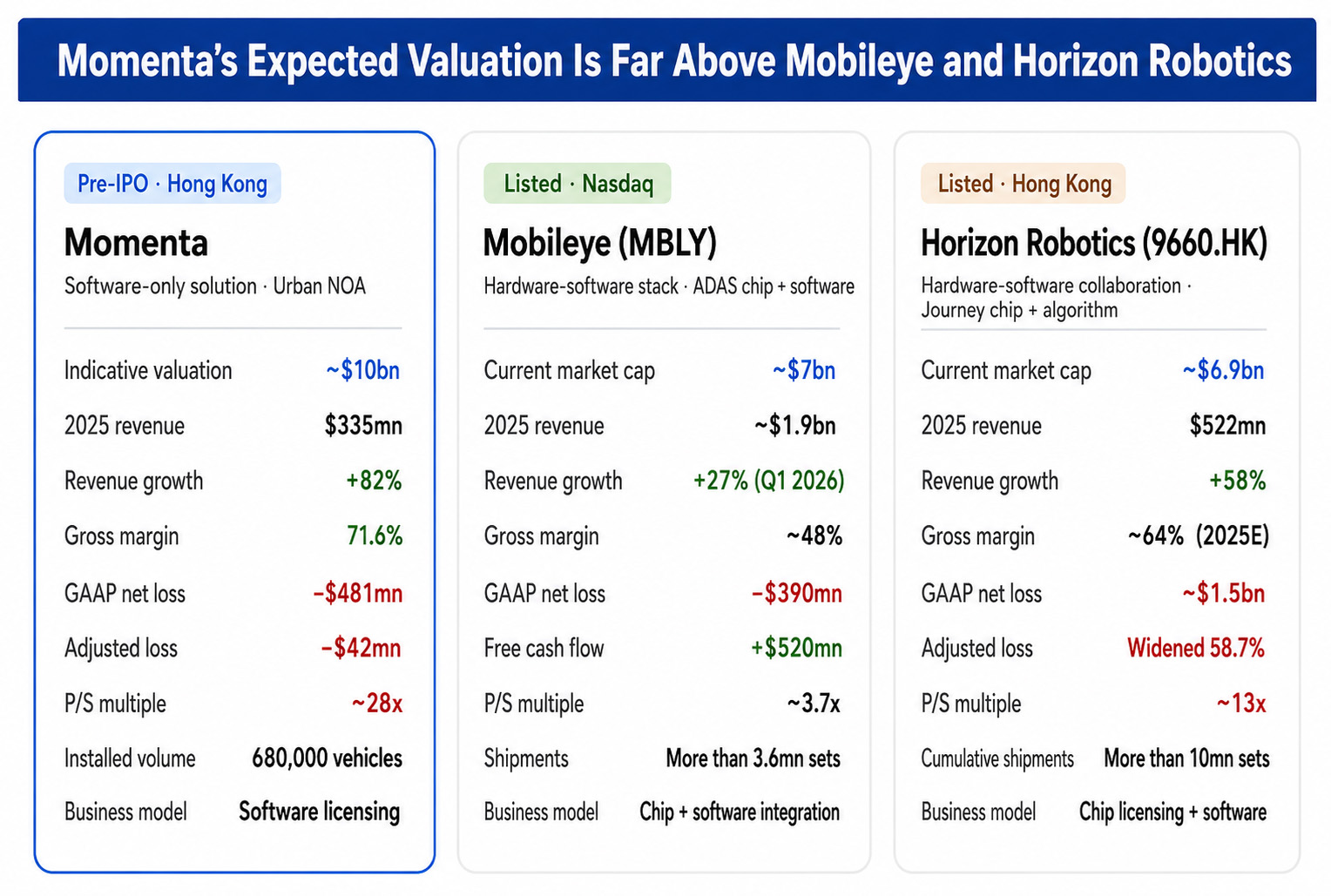

At an expected valuation near $100 billion, Momenta would trade at roughly 28x price-to-sales based on 2025 revenue of 2.41 billion yuan.

By comparison, Mobileye trades at roughly 3.7x sales, while Horizon Robotics is valued at around 13x sales based on a 2025 revenue base of 3.758 billion yuan.

Converted into US dollars, Momenta’s valuation implies approximately $9,444,000,000 relative to its current revenue scale.

Gross margins of 71.6% place it ahead of both Horizon Robotics (~64%) and Mobileye (~48%), supporting a premium software-style multiple. Yet scale dynamics remain markedly different, with Mobileye and Horizon benefiting from far larger installed bases.

Between profitability and scale: the open questions ahead

The company sits between two narratives: improving unit economics driven by software licensing, and persistent heavy investment required for autonomy development.

Key variables include sustained R&D discipline, the timing of meaningful Robotaxi revenue, and whether automakers continue to expand reliance on external autonomous driving platforms rather than shifting in-house.

For investors, the IPO marks not a conclusion but the beginning of a public market test: whether Momenta’s rapid margin expansion can survive exposure to cyclical automotive demand and intensifying competition in China’s fast-consolidating autonomous driving ecosystem.