While much of the attention around China's car industry remains fixed on vehicle-price wars and intelligent-vehicle features, a deeper restructuring is moving through the supply chain.

The consolidation wave has moved upstream

Auto-parts makers are using acquisitions to secure technology, customers and manufacturing capacity before the next phase of competition hardens.

According to a report by Economic Information Daily citing Tonghuashun iFinD data, 67 listed automotive companies had disclosed merger or acquisition announcements this year as of June 12, based on first announcement dates. Auto-parts companies have been the main actors.

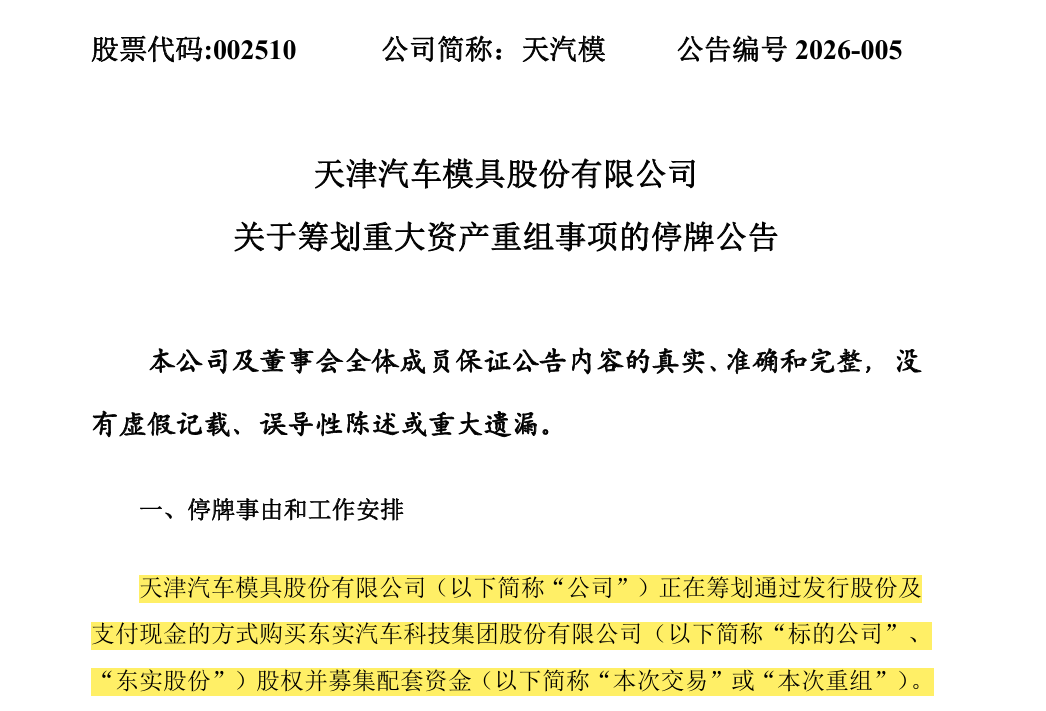

The deals are large and increasingly ambitious. Bethel Automotive Safety Systems agreed to spend about $1.56 billion for a 50.97% stake in Yubei Steering. Tianjin Motor Dies plans to pay roughly $2.55 billion for 60% of Dongshi, a target whose revenue is nearly twice its own. Joyson Electronics is spending about $3.50 billion to raise its holding in Joyson Safety, while Viti Electronics is attempting a cash acquisition of Jiuxing Precision for about $1.53 billion.

What stands out is the number of smaller companies trying to absorb larger or more profitable targets. These are not passive financial investments. They are control deals.

Control has become the strategic prize

The pattern across the first half of the year is clear: listed suppliers are no longer content to take minority stakes and share in future dividends. They want decision-making power.

Tianjin Motor Dies is a useful example. Under a restructuring plan disclosed on June 8, the company intends to use a mix of shares and cash to acquire 60% of Dongshi. It already holds 25%, so the transaction would lift its stake to 85% and give it deep control over a major parts supplier.

The purpose is broader than consolidating revenue. Tianjin Motor Dies wants to complete its product chain, expand its customer base and regional footprint, and control the industrial coordination between moulds and parts. In a slower market, the ability to direct technology road maps and production resources matters more than a financial stake.

Bethel is following a similar path. It announced its plan in late February, cleared antitrust review in May and completed delivery in June, taking 50.97% of Yubei Steering at an implied total valuation of about $3.06 billion. Yubei generates more than $418 million in annual revenue and brings mass-production capacity across C-EPS, DP-EPS and R-EPS electric steering products. For Bethel, the prize is faster progress toward steer-by-wire and a fuller electric-steering portfolio.

Other companies are tightening control over businesses they already hold. Joyson Electronics plans to acquire a further 12.42% of Anhui Joyson Safety from an advanced manufacturing fund for about $3.50 billion, lifting its stake from 57.12% to 69.54%. Ruili Kormee is buying the remaining 16% of Wuhan Kedes for about $2.23 million, while Mingke Precision is paying about $20.06 million for 53.25% of Anhui Shuangjun to move from single components toward higher-margin system solutions.

Why smaller buyers are taking bigger swings

The logic behind these bold deals is not that acquirers have unusually large cash piles. It is that certain targets have become difficult to replace. Technology, customer access and manufacturing layout can be worth more than a simple comparison of balance-sheet size.

Dongshi shows why. At the transaction reference date, Dongshi's total assets were about $855 million, nearly level with Tianjin Motor Dies' roughly $881 million. Its net assets were about $385 million, higher than the buyer's roughly $351 million. Its 2025 revenue was almost twice that of Tianjin Motor Dies. On scale alone, the target looks too large.

Yet Dongshi is one of China's few suppliers with large-scale support for both commercial vehicles and passenger cars, covering body, chassis and powertrain systems. It generated revenue of about $507 million in 2024 and $625 million in 2025, with net profit attributable to the parent of about $52 million and $49 million. For a buyer that began in moulds, Dongshi offers a missing link in a more complete parts chain.

Viti Electronics is making a different version of the same bet. The auto-electronics company, already loss-making in the first quarter of 2026, plans to acquire 90.97% of Jiuxing Precision in cash. The target is valued at about $167 million, with an appraisal uplift of 423.67%. Viti's own annual profit has been modest, while Jiuxing earns more than $12.5 million a year. The deal relies on about $97.5 million of acquisition financing and is intended to create a second growth engine.

These transactions are appearing now because the consolidation window has opened. Industry data put the gross margin of China's A-share auto-parts sector at about 18.5% in 2025, down 0.5 percentage points from 2024 and more than three points below the pre-EV era before 2019. Legacy businesses are earning less, while electrification and intelligent-vehicle projects require heavy spending. Lower valuations give strategic buyers a chance to move.

The hard work begins after the signing

Buying control is only the first step. The more difficult task is absorbing the target, reducing overlap, diversifying customers and turning promised synergy into operating results.

Joyson Electronics offers a cautionary history. Since its backdoor listing in 2011, the company has completed a series of major overseas acquisitions, including Germany's PREH, America's KSS and assets from Japan's Takata. The transactions helped lift revenue quickly, but also left debt, goodwill and integration burdens. For smaller acquirers trying to digest larger targets, the management challenge can be even more severe.

Dongshi itself carries issues that Tianjin Motor Dies will need to solve. It has long relied heavily on Dongfeng-related customers. Accounts receivable stood at about $181 million in 2024 and $169 million in 2025, a meaningful share of total assets. Customer concentration was one of the reasons Dongshi's earlier IPO attempt failed. The acquisition will only create lasting value if the buyer can broaden the customer base and improve cash collection.

Viti faces a sharper financial test. One director voted against the acquisition plan, citing the risks of an all-cash, high-ratio purchase and the debt load that would follow the acquisition financing. Jiuxing itself is not without pressure: by the end of October 2025, it had total liabilities of about $95 million and a debt-to-asset ratio of 65.98%. In the first quarter of 2026, revenue fell 26.89% year on year and net profit dropped 60.21%. The forecast of about $18.4 million in annual net operating profit after tax is far from guaranteed.

Scale alone will not decide the winners

CICC has argued that traditional sectors such as auto parts are using horizontal integration and strategic cooperation to optimise industrial structures and improve resource allocation. That is true, but acquisitions are easier to announce than to integrate.

Chinese suppliers have already grown through dealmaking. From 2012 to 2025, the number of Chinese companies in the global top 100 auto-parts suppliers rose from one to 15, with CATL, Yanfeng, Joyson Electronics and CITIC Dicastal entering the global top 50. Scale jumps have often come from acquisitions.

The current wave is different because the buyers are chasing control in a tougher market. Capital can secure voting power, but it cannot guarantee industrial coordination. The real value of these deals will be decided in daily operations: product integration, customer expansion, working-capital discipline and the ability to turn acquired technology into orders.