China’s car market has rarely looked busier. New models are arriving at a pace of more than three a day, electric-vehicle penetration is hitting fresh highs and automakers are still fighting for share in the world’s most competitive auto market.

Behind the showrooms and launch events, the industry is showing signs of strain. A surge in supply, a split pricing cycle between electric and petrol cars, and weakening consumer confidence are putting growing pressure on dealers — the part of the auto chain least able to absorb the shock.

In the first five months of 2026, 544 new passenger-vehicle models or variants were launched in China, equal to an average of 108.4 a month, or 3.6 a day. The pace accelerated sharply after the Lunar New Year lull, with 133 launches in March and 174 in April alone.

The flood of products reflects a familiar strategy in China’s auto industry: use a wide model line-up to capture attention in a slowing market. Yet the approach is losing force. Passenger-car retail sales fell 22.1% year on year in May to 1.51 million units, while sales in the first five months dropped 19.5% to 7.1 million units. The market has improved slightly month on month, but a sustained recovery has yet to appear.

The Limits of the “Model Sea” Strategy

Automakers are still pushing new vehicles into the market at full speed, from complete redesigns to annual updates and small trim-level revisions. In a market where growth is harder to find, each company is trying to defend visibility and hold consumer attention.

The problem is that more models no longer guarantee more demand. In the first four months of the year, the number of models selling more than 10,000 units a month peaked at just 46, and at weaker points fell below 30. Many launches are failing to gain meaningful traction after their debut, suggesting that China’s once-effective “model sea” strategy is producing diminishing returns.

The result is a more crowded market with fewer clear winners. As consumers wait for deeper discounts, better technology or the next new model, automakers are finding it harder to convert product launches into stable sales.

EV Prices Rise as Petrol Cars Keep Cutting

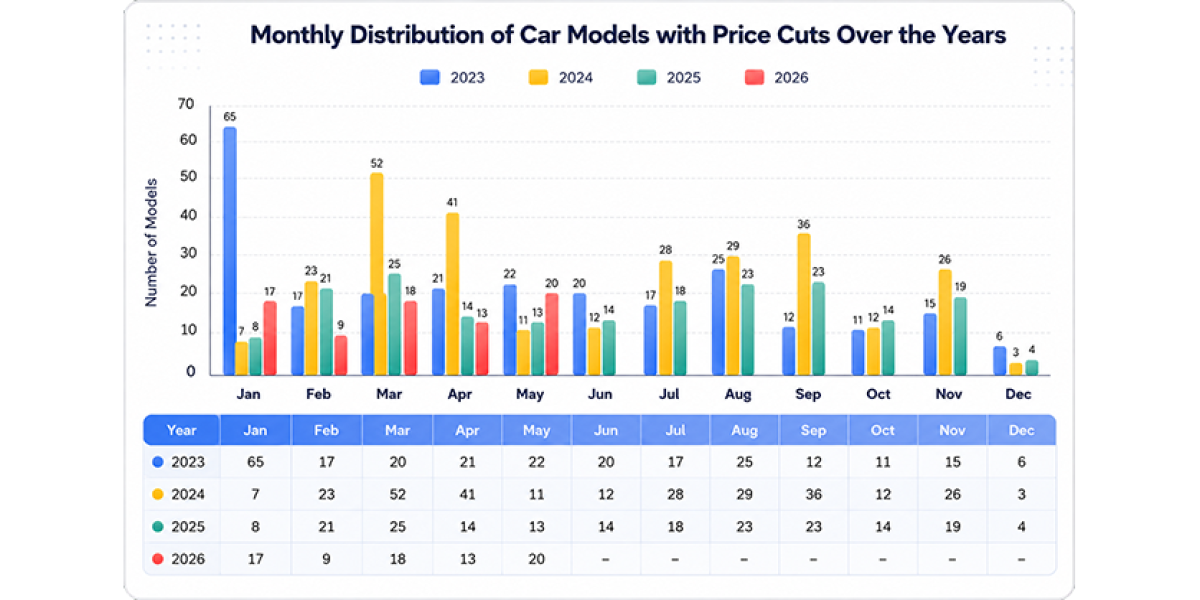

China’s price war has also entered a more complicated phase. In 2025, more than 100 models saw price cuts as carmakers competed aggressively for volume. In 2026, the market has split in two.

According to data released on June 7 by Cui Dongshu, secretary-general of the China Passenger Car Association, 77 models were discounted in the first five months of the year. Petrol cars accounted for 32 of them, an increase from the same period a year earlier. At the same time, more than a dozen new-energy-vehicle makers have raised prices or reduced incentives.

The reversal has been driven largely by rising input costs. From March to June, prices for automotive-grade memory chips reportedly rose by about 180%, as global demand for AI computing capacity diverted advanced production from major memory-chip suppliers toward servers. The chip squeeze alone is estimated to have added close to $1,000 to the cost of each vehicle.

Battery materials are adding to the pressure. Lithium carbonate prices have risen from about $18,000 a tonne at the start of the year to more than $30,000, increasing costs for electric-vehicle producers. Brands including BYD, Nio, Xiaomi, Zeekr, Changan Qiyuan and Huawei-backed Harmony Intelligent Mobility have adjusted prices on popular models, with increases ranging from less than $1,000 to more than $1,000.

Petrol cars are moving in the opposite direction. In May, 20 models introduced fresh discounts, including seven pure petrol models and seven plug-in hybrids. The average petrol model involved in the latest round of cuts was priced at about $25,000, with an average discount of about $4,000, equal to a reduction of 14.9%.

Promotional pressure in the petrol-car market has remained near 23% for nine consecutive months. For joint-venture petrol brands, the promotion rate was 22.4%. The message is clear: EV makers are trying to protect margins from rising costs, while petrol-car makers are cutting prices to defend shrinking demand.

Dealers Are Absorbing the Damage

The burden is landing most heavily on dealers. China’s retail channels are being squeezed by inventory, falling margins and delayed rebate payments from manufacturers.

A national dealer survey for 2025 showed that only 23.5% of stores were profitable, while 55.7% were lossmaking. Price inversions — where vehicles are sold below the effective cost to the dealer — have become common. For many retailers, higher sales no longer mean healthier cash flow.

The latest ranking of China’s top 100 dealership groups points to the same pressure. Their combined revenue fell 8.82% to about $254 billion, even though new-car sales in the first five months declined only 1.7% to 7.88 million units. The gap suggests that per-vehicle profitability has weakened sharply as discounts and price inversions eat into margins.

Inventory is another source of stress. China’s auto dealer inventory warning index reached 57.9% in May, up 5.2 percentage points from a year earlier and marking the third consecutive month of year-on-year increases. In April, 17 mainstream brands had inventory depth of more than two months, tying up large amounts of dealer working capital.

The rebate cycle is making matters worse. The China Automobile Dealers Association has said traditional carmakers have yet to move fully away from a production-led model, while manufacturer rebates now take more than 70 days on average to be paid. That delay leaves dealers financing the gap at a time when retail demand remains weak.

The physical network is already contracting. China’s 4S dealership base has shrunk for two consecutive years. In 2025 alone, the market recorded a net reduction of about 1,480 stores, while 2,749 outlets exited their networks. Closures have continued to accelerate in 2026, raising questions about the stability of the industry’s offline sales system.

Weak Confidence Is the Hardest Problem

The pressure on dealers also reflects a broader problem: consumers remain cautious. A survey by the China Automobile Dealers Association found that more than 80% of dealers saw weak purchase intent among consumers, while only 13.5% believed the wait-and-see mood had eased.

That creates a contradiction at the heart of the market. Supply is expanding rapidly, automakers are adjusting prices, and new-energy vehicles are taking a record share of sales. In May, NEV retail penetration reached 62.9%, meaning more than six out of every ten new passenger vehicles sold in China were electrified. Petrol-car sales, by contrast, fell 39% year on year, with independent-brand petrol models down 39%, mainstream joint-venture petrol models down 41%, and luxury petrol models down 31%.

The shift from petrol to electric cars is not the problem in itself. Nor is the large number of new models. The deeper risk is that supply-side ambition and the industry’s price-war habits are squeezing the channels that connect automakers with consumers, while confidence at the retail end has yet to recover.

Dealers are often the quietest participants in China’s auto upheaval, but they remain one of the most important. If the dealer network continues to weaken, the industry’s foundation will become more fragile. The first five months of 2026 show that China’s auto market is not short of launches, technology or headline numbers. What it needs is a better balance between supply chains, sales channels and consumer demand.