China’s car industry is launching new vehicles at a pace more commonly associated with consumer electronics. In the first half of 2026, about 630 new or updated models reached the market — more than three a day. Over the same period, China’s smartphone market introduced just 157 new devices.

The flood of launches suggests relentless innovation. The sales figures tell a different story. Passenger-car retail sales fell 22.1% year on year to 1.51 million units in May, while sales in the first five months dropped 19.5% to 7.099 million. Supply is accelerating even as demand contracts.

That widening gap has exposed one of the defining problems of China’s electric-vehicle boom: speed, once the industry’s greatest advantage, is increasingly becoming a source of waste, falling residual values and weaker consumer confidence.

The Illusion Behind 630 New Cars

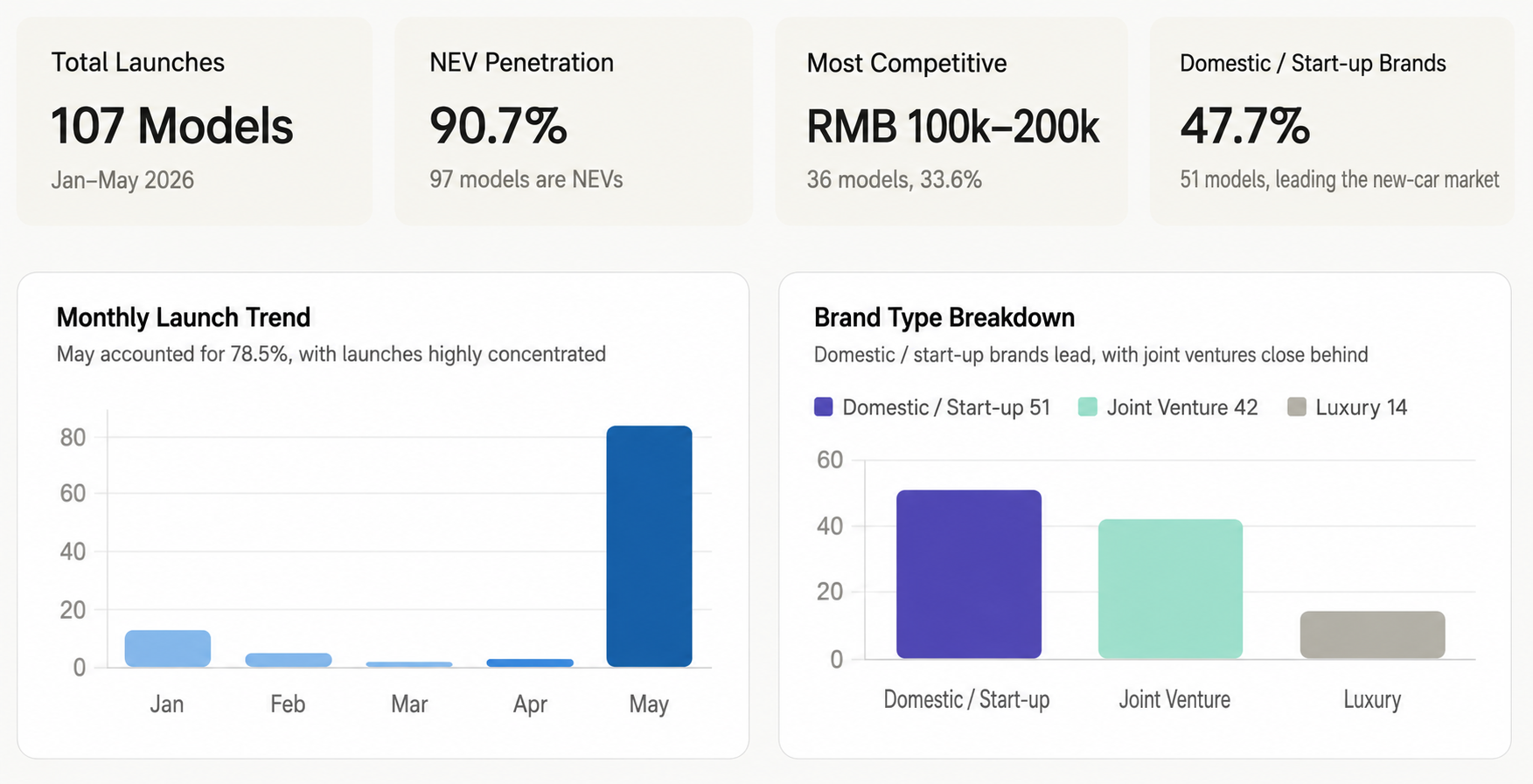

Roughly 550 vehicles were launched in China between January and May, followed by about 80 more in June. Yet only 107 of the models introduced during the first five months were genuinely new vehicles built on fresh architectures or full generational replacements. Fewer than one in five represented a substantial product change.

The rest largely consisted of annual updates, revised equipment packages, new paint options or limited-edition collaborations. In a market where every adjustment can be promoted as a launch, the headline number says more about marketing pressure than engineering output.

Sales concentration is even more severe. Based on retail data for the first five months, fewer than 30 passenger-car nameplates were consistently selling more than 10,000 units a month. Only a small fraction of the hundreds of newly introduced models entered the market’s mainstream sales tier.

Many products are fading almost as soon as they arrive. Industry observers have begun referring to a “three-month curse”: a vehicle attracts attention at launch, only to lose momentum within a quarter as a fresh wave of similarly priced competitors takes over showroom space and online discussion.

Carmakers continue launching because standing still is often seen as more dangerous than adding another model. China’s new-energy vehicle penetration rate reached 62.9% in May, but the market is no longer expanding fast enough to support every brand and product line. Companies fear that without a new vehicle, a new feature or a new price point, rivals will capture the attention of potential buyers.

The pressure is particularly acute for electric-vehicle start-ups that have yet to reach profitability. New models provide fresh narratives for investors, dealers and consumers. Without launches, there are fewer headlines, fewer showroom visits and fewer reasons for capital markets to believe that growth will continue.

Yet volume of choice is not the same as quality of choice. Faced with hundreds of overlapping vehicles, buyers are increasingly struggling to distinguish meaningful improvements from cosmetic changes. The result is not always a purchase. Many consumers simply delay, convinced that a better-equipped or cheaper model will arrive within months.

Rapid Launches Are Undermining Used-Car Values

The same cycle is putting pressure on China’s used-car market. When new models arrive every day, recent vehicles quickly appear outdated. Buyers prefer the latest version, dealers become cautious about taking older cars into stock, and inventory takes longer to sell.

Average turnover periods for used vehicles have reportedly stretched from about 15 days to between 30 and 45 days. Higher financing and storage costs force dealers to lower purchase prices, transferring much of the loss to existing owners.

Three-year residual values for several popular plug-in hybrid SUVs have fallen from roughly 58% to about 52%. Some models that undergo frequent updates or sharp price cuts can lose as much as 40% of their value within a year.

This depreciation feeds back into the new-car market. Consumers who expect a vehicle to lose value immediately after purchase become less willing to commit, particularly when the next version may offer more equipment at a lower price.

Why the Average EV Looks Only 1.8 Years Old

One frequently cited statistic says the average age of a new-energy vehicle in China is just 1.8 years. That has sometimes been interpreted as evidence that EV owners replace their cars almost as often as smartphones. The reality is more complicated.

China sold more than 12.8 million new-energy passenger vehicles in 2025. Those new registrations accounted for close to 30% of the existing fleet, pulling down the average age because the market itself is still young.

Used-car transactions offer a clearer measure of ownership cycles. The average new-energy vehicle traded in China in 2025 was 3.4 years old, according to industry data. In practice, EV owners tend to replace their vehicles after three to five years. That is still faster than the six-to-eight-year cycle common for combustion-engine cars, but far from an 18-month replacement pattern.

The gap reflects a fundamental shift in what a car has become. Combustion vehicles are built around mechanical systems whose development cycles can run for five to eight years. A decade-old engine or gearbox may still deliver an experience broadly comparable with newer models.

Electric cars depend more heavily on batteries, processors, software and driver-assistance systems. Those technologies are evolving on 18-to-24-month cycles. A vehicle bought only two or three years ago can already feel behind if its computing platform cannot support the latest infotainment software or if newer rivals offer more capable assisted-driving functions.

That creates a self-reinforcing loop. Frequent launches shorten the commercial life of existing models. Faster depreciation encourages owners to sell earlier. A growing supply of nearly new vehicles then pushes residual values down further.

Consumer complaints show how quickly frustration is rising. Between January and November 2025, disputes linked to rapid model replacement reached 39,300 cases, around 82 times the level recorded a year earlier. Common complaints included vehicles becoming “old models” soon after delivery and newer versions receiving more equipment at lower prices.

New Safety Rules Will Force the Industry to Slow Down

China’s regulatory response is arriving in 2026, a year in which 82 national automotive standards are scheduled to take effect, including 26 mandatory rules.

Two major standards covering electric-vehicle battery safety and overall EV safety took effect on July 1. The battery rules move beyond requiring an alert before thermal runaway. Under the new tests, battery packs are expected to avoid fire or explosion during thermal propagation assessments.

The standard includes seven cell-level tests and 17 battery-pack or system tests, as well as new requirements covering underbody impact and safety after repeated fast charging. The broader vehicle rules also require an independent physical mechanism capable of disconnecting the high-voltage circuit after a serious collision, even if software or in-car communications fail.

These measures amount to a regulatory correction after years in which speed-to-market often took priority over long validation cycles. Marketing concepts, design features and software promises moved faster than engineering verification, leaving safety risks that regulators are now attempting to address.

Compliance will also accelerate consolidation. Meeting the new battery standard alone could add roughly $1,000 to the cost of each vehicle, before accounting for additional testing and development time. Smaller brands without proprietary technology, stable suppliers or deep financial reserves will find it harder to keep launching products at the same pace.

China’s EV Market Is Reaching the Limits of Expansion by Volume

The financial case for endless launches is becoming increasingly difficult to defend. China’s automotive manufacturing profit margin fell to 3.2% in the first quarter of 2026, a record low and about two percentage points below the average for large industrial companies.

Industry sales margins also declined from 6.1% to 3.2%, while average gross profit per vehicle fell from roughly $3,000 to $2,000. In that environment, adding more models spreads engineering, manufacturing and marketing budgets across products that may never reach meaningful scale.

Most of the 630 vehicles introduced in the first half were not creating new demand. They were dividing existing demand into smaller segments, accelerating depreciation and weakening trust among buyers who increasingly expect rapid price cuts or replacement models.

Several manufacturers are already narrowing their line-ups and concentrating resources on fewer vehicles. That shift may make 2026 the year in which China’s electric-car industry finally begins to slow its product cycle.

The next stage of competition will be less about how many vehicles a company can launch and more about whether each one can survive. For an industry that has spent years proving itself through speed and scale, winning trust through durability, safety and product discipline may be the harder test.