The era of relentless price cuts in China's car market is running into a more stubborn force: the cost of the supply chain.

The End of Easy Discounts

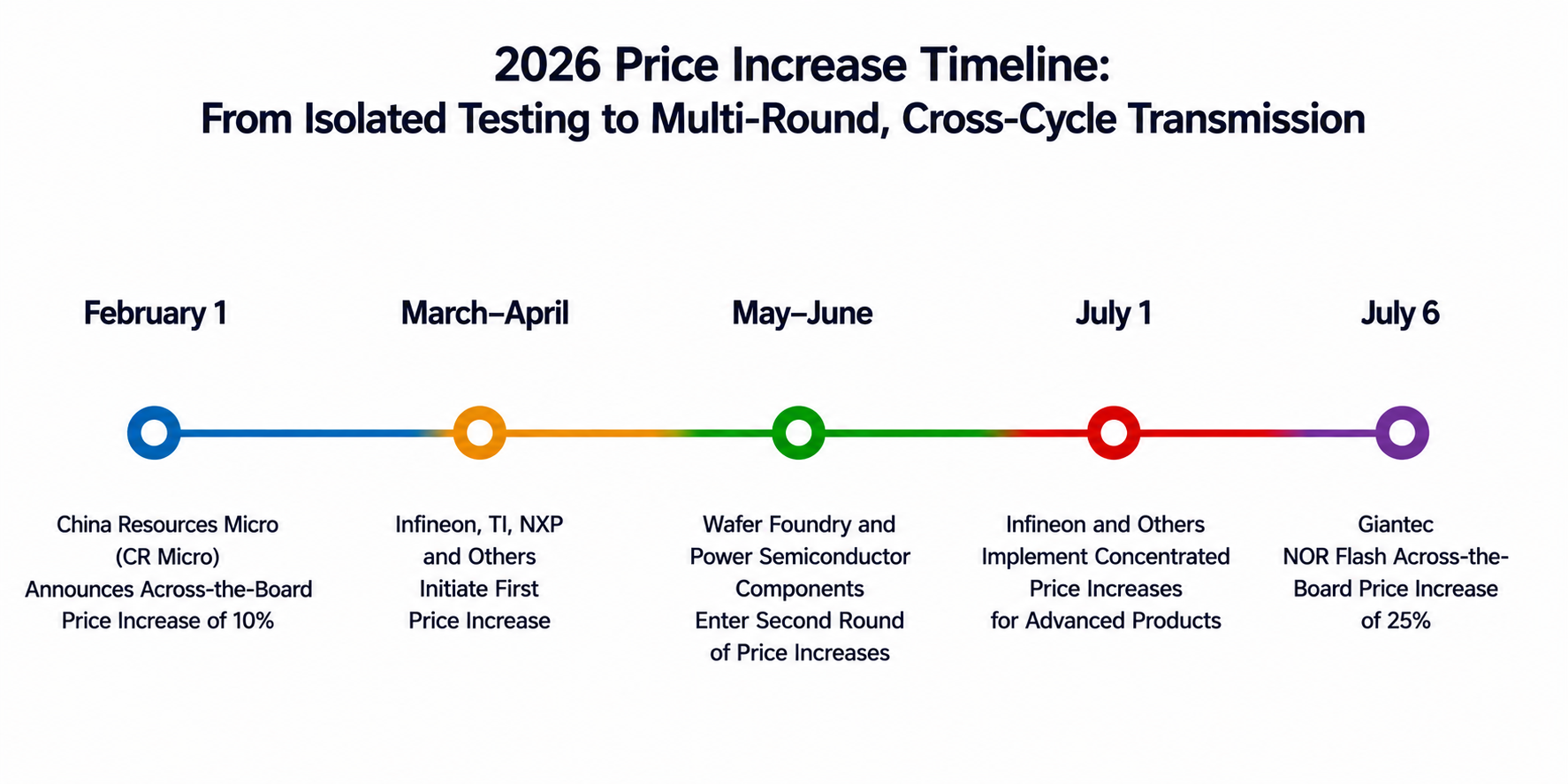

As July began, a new round of semiconductor price increases swept across the automotive sector. Nearly 20 chipmakers, including Siengine Technology, StarPower Semiconductor, Yangjie Technology and GigaDevice-linked Juchen Semiconductor, have issued price adjustment notices. Siengine said third-quarter product prices would rise by 15% to 25%, Yangjie lifted prices across its portfolio by 10% to 15%, and Juchen raised prices for its Nor Flash products by 25%. StarPower said higher wafer, metal and packaging-material costs had moved beyond what the company could absorb internally.

Global suppliers are moving in the same direction. Infineon raised prices from July 1 on power-management chips for AI servers, automotive-grade IGBTs and high-voltage MOSFETs by 10% to 20%. Texas Instruments and STMicroelectronics have also started a second round of increases this year, covering signal-chain chips, analog power components, data-centre semiconductors and automotive power devices. High-voltage power chips and power MOSFETs linked to AI data centres are seeing some of the steepest increases, typically 15% to 25%.

The result is a market that is shifting from selective shortages to a broader inflation cycle. For carmakers, the timing could hardly be worse.

China's passenger-car market remains under pressure. According to industry data cited in the original report, retail sales reached 7.11 million units in the first five months of 2026, down 19% from a year earlier. Sector profit fell 20% to about $20 billion, while the industry's profit margin dropped to 3.4%, the weakest level for the period in almost a decade.

Carmakers are trapped between rising component costs and consumers trained to expect discounts. The question is no longer how far prices can fall. It is how long the industry can absorb the bill.

AI Is Now Competing With Cars for Chips

The latest wave of price increases starts with the most powerful demand force in the technology market: artificial intelligence.

An AI server can consume more than 1,200 watts, compared with roughly 300 watts for a traditional server. It can also use three to five times as many power semiconductors. That has pushed demand sharply higher for upstream power-management chips, precisely the type of components that also matter to electric vehicles and intelligent-driving systems.

Infineon Chief Executive Jochen Hanebeck told investors in May that demand for AI data-centre power solutions remained strong, with the company expecting AI-market revenue of 2.5 billion euros in fiscal 2027. Texas Instruments' data-centre revenue rose 90% year on year in the first quarter, while its overall revenue has grown sequentially for eight straight quarters.

The squeeze is even tighter in memory. Samsung, SK Hynix and Micron have shifted much of their advanced capacity toward HBM and high-end DDR5 memory used in AI computing. Automotive-grade memory has been pushed down the priority list. The auto industry accounts for less than 10% of global DRAM demand, leaving it with less leverage than AI infrastructure or consumer electronics when suppliers allocate capacity.

That imbalance has sent memory prices sharply higher. In the first quarter of 2026, contract prices for general-purpose DRAM rose 90% to 95% quarter on quarter, while NAND flash contract prices climbed 55% to 60%, both record increases.

Wafer foundry pricing is adding another layer of pressure. Eight-inch mature-node capacity has tightened as AI-related power-device orders rise and as foundries including TSMC and Samsung trim output in some areas. Average foundry prices for those processes have increased by 5% to 15%, while 12-inch mature-node processes are up 5% to 10%. TrendForce expects the pricing effect in mature processes to extend into 2027.

Raw materials are moving in the same direction. Copper rose from about $13,000 a tonne at the end of March to roughly $15,000 by the end of May. Tin has been trading around $56,000 to $61,000 a tonne. Lithium carbonate, a key battery material, jumped from about $10,000 a tonne at the end of 2025 to roughly $28,000 by mid-May 2026. These increases are now feeding into chip production costs.

Chinese suppliers have followed the same pattern. Yangjie raised prices in March and then lifted its entire product range again in July. China Resources Microelectronics moved first in February with increases starting at 10%, while Silan Microelectronics and NCE Power also joined the adjustment cycle. After an initial wave of price notices in the first half, a second round is now spreading across the industry.

For Carmakers, Both Price Cuts and Price Rises Carry Risks

Semiconductors are not the only problem. They are landing on an industry already facing weaker volumes and thinner margins.

Retail sales of passenger cars reached 913,000 units in the first three weeks of June, down 23% year on year, according to the China Passenger Car Association data cited in the source article. Some industry estimates now point to a full-year decline of 15% to 20% in domestic retail sales. The contraction in internal-combustion vehicles remains the main drag: their market share fell to 37.1% in May, and the decline in petrol-car sales accounted for 82% of the total drop in passenger-car volume.

Profitability is deteriorating at the same time. The auto industry's profit margin fell to 3.2% in the first quarter of 2026, a near-decade low, and stood at 3.4% for the first five months. That is well below the 4.9% average for large industrial companies and the 6.1% level for downstream industrial sectors. Margins have been falling for three consecutive years, from 4.3% in 2024 to 4.1% in 2025, before sliding again in 2026.

Chip and raw-material inflation is now adding thousands of dollars to vehicle costs. Industry estimates cited in the article suggest that upstream semiconductor and material increases are adding more than $1,000 to the cost of some vehicles, with an implied effect on retail pricing of roughly $2,000.

Zhang Xinghai, chairman of Seres Group, gave a more specific example at a forum in Chongqing. He said memory-chip prices had more than quadrupled, while lithium carbonate had risen from about $11,000 a tonne to roughly $25,000. For Aito vehicles, he said average per-car costs had increased by about $2,000 to $3,000. UBS has estimated that memory-chip inflation alone could add roughly $1,000 to the cost of a high-end assisted-driving model.

The industry-wide numbers show how narrow the room for manoeuvre has become. In the first five months of the year, revenue per vehicle in China's auto manufacturing industry was about $48,000, while cost per vehicle reached roughly $42,000, up 6.7% from a year earlier. Great Wall Motor President Mu Feng put the dilemma bluntly when he said the company was not seeking excessive profit, but still needed to make a profit.

The pressure may last. New global wafer capacity typically takes at least 18 months to build and ramp up. Demand from AI computing and electrification is still expanding. That leaves little near-term relief for automakers caught between weaker retail demand and more expensive components.

Consumers Are Turning Against the Price War

The market is also showing signs that price cuts are losing their power.

McKinsey's 2026 China Automotive Consumer Insights report, released in May, found that the price war has begun to damage consumer confidence. Among owners who bought a vehicle in the past year, 22.2% viewed the price war negatively, compared with 16.5% who viewed it positively. The fear of buying a car only to see its price cut soon after has started to weigh on purchase decisions.

Technology upgrades and better equipment tell a different story. Their net positive effect on buying decisions reached 20.7%, almost double last year's level. Buyers are becoming less willing to pay simply for a lower sticker price. They are more willing to pay for visible value.

Price increases have already begun. More than 15 new-energy vehicle companies have announced price rises or reduced terminal discounts since the start of the year, according to incomplete industry tracking. Traditional petrol-car brands are still cutting prices, but EV makers are increasingly moving in the opposite direction. The reason is uncomfortable: the more intelligent a vehicle becomes, the more chips it uses, and the heavier its cost burden becomes.

The Next Battle Is Supply Chain Control

If the price war is running out of road, the next battleground is the supply chain.

At the retail level, carmakers are cutting discounts, nudging up prices and reducing subsidies to protect margins. In procurement, several leading manufacturers have begun signing long-term supply agreements with overseas memory-chip makers to secure capacity for the next one to two years. Some are also building three to six months of safety inventory.

The deeper strategic shift is toward domestic substitution and in-house chip development. For China's automakers, 2026 is shaping up as a key year for self-developed intelligent-driving chips. The economics are clear. Developing a high-compute assisted-driving chip can cost hundreds of millions of dollars, but once it reaches mass production, the chip cost per vehicle can fall sharply.

Wang Xia, chairman of the automotive committee of the China Council for the Promotion of International Trade, summed up the industry's new reality: sales without profit are little more than an empty numbers game. When every chip and every tonne of raw material is becoming more expensive, volume bought with discounts becomes harder to defend.

The July semiconductor price increases are not the start of the cycle, and they are unlikely to be the end. With AI computing demand still rising and wafer capacity expanding slowly, the chip inflation cycle could last for more than a year. For China's carmakers, the era of the price war is giving way to a supply-chain cost war. The companies that can localise critical components, secure capacity and cut technology costs first will be the ones most likely to survive the next round of industry consolidation.