China's automotive industry has reached another defining moment. June delivery figures, which effectively closed the books on the first half of 2026, reveal a market becoming increasingly divided rather than uniformly competitive.

Instead of one industry moving in the same direction, three distinct races are emerging. Electric vehicle startups are entering a period of consolidation after years of rapid expansion. Established Chinese manufacturers are attempting to balance record production with the complex transition from internal-combustion vehicles to electrification. Foreign joint ventures, once the undisputed leaders of the market, are quietly rebuilding themselves around China's technology ecosystem.

The numbers themselves are impressive. Several manufacturers reported record deliveries, exports continue to accelerate and electric vehicles are capturing a growing share of the market. Yet the figures also tell a broader story. China's auto industry is moving beyond a phase where rapid demand could lift almost every participant. Competitive advantages are becoming increasingly concentrated among companies capable of combining manufacturing scale, software capability, supply-chain control and faster product development.

For investors, suppliers and global automakers, the first-half scorecard offers something more valuable than another collection of monthly sales statistics. It provides an early look at how the competitive hierarchy inside the world's largest automotive market is evolving—and, increasingly, how the future structure of the global automotive industry may be shaped.

China's EV Startups Are Entering an Era of Consolidation

Only a few years ago, China's electric vehicle startup sector was defined by fierce competition among dozens of ambitious challengers. Success often depended on attracting capital, launching new products quickly and maintaining delivery momentum. The first-half results suggest that phase is giving way to something very different.

Scale has become the industry's most valuable asset, and a small group of manufacturers is beginning to separate itself from the rest of the market.

Leapmotor has become the clearest example of that transition. The company delivered 93,376 vehicles in June, including overseas shipments, representing year-on-year growth of 95%. First-half deliveries reached 356,487 units, placing the company firmly at the top of China's startup EV sector.

The achievement reflects more than another strong sales month. Annual deliveries stood at only around 43,000 vehicles in 2021. Four years later, Leapmotor is approaching the 100,000-unit monthly threshold, illustrating one of the fastest growth trajectories among global electric vehicle manufacturers.

The company's rise also highlights an increasingly concentrated market structure. Leapmotor now accounts for more than one-third of deliveries among China's leading startup brands, suggesting the sector is moving away from fragmented competition toward one dominated by a handful of large-volume manufacturers. Greater scale allows companies to negotiate lower component costs, invest more heavily in software development and accelerate overseas expansion, advantages that become increasingly difficult for smaller rivals to replicate.

NIO also reported one of its strongest performances in recent years. June deliveries reached 40,597 vehicles, an increase of 62.9% from a year earlier, while first-half deliveries climbed to 191,123 units, equivalent to roughly 42% of the company's annual target.

The improvement reflects broader momentum across the group's expanding brand portfolio. The core NIO brand remained the largest contributor, while ONVO continued strengthening its position in the family-oriented market. Firefly, NIO's newest compact EV brand, recorded particularly rapid growth as production accelerated during the first half.

Chairman William Li has repeatedly described 2026 as one of the company's most demanding years despite improving deliveries. His comments underline an important shift across the sector. Investors are becoming less interested in headline volume alone and increasingly focused on profitability, operational discipline and sustainable growth.

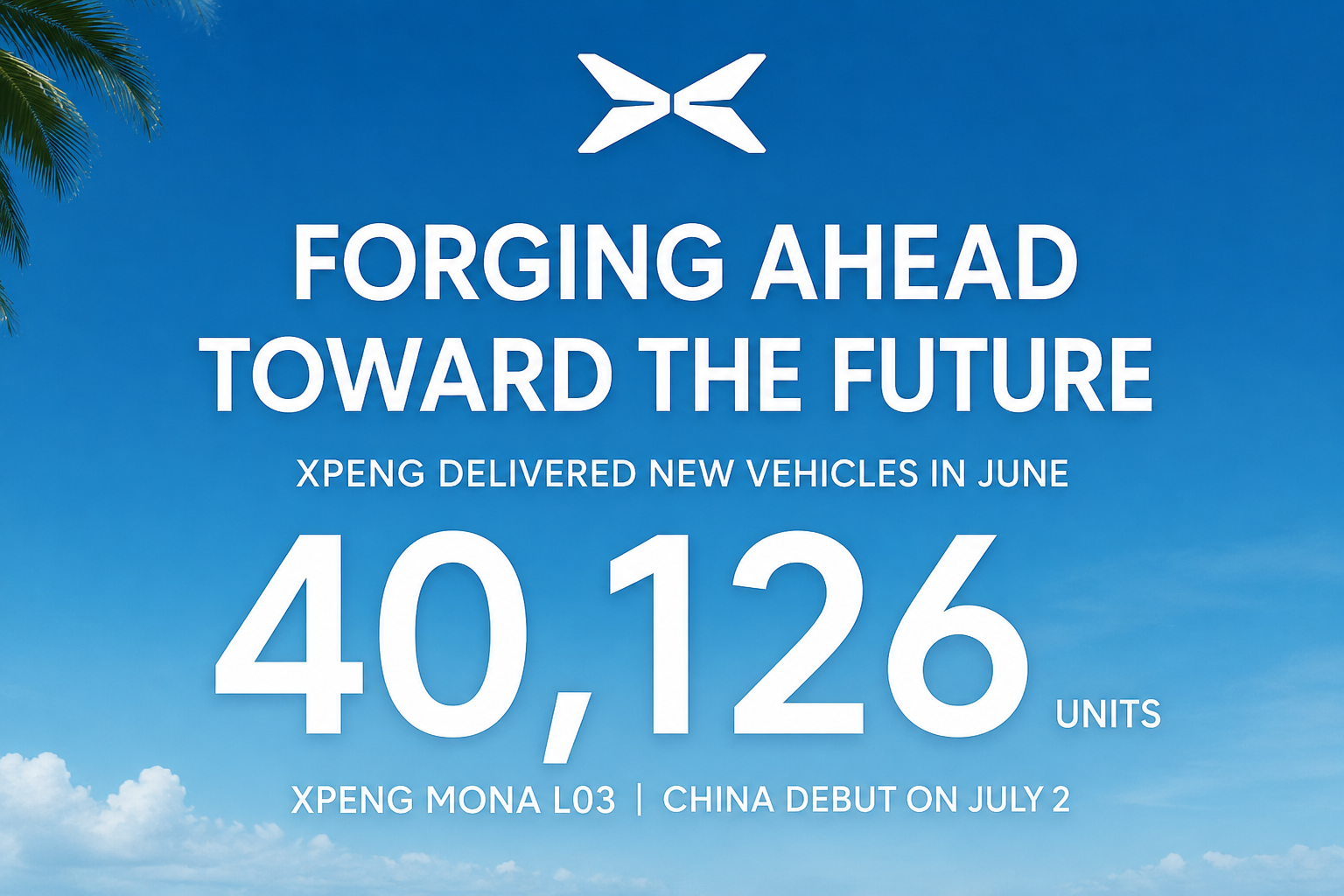

XPeng maintained deliveries above the 40,000-unit mark, reporting 40,126 vehicles in June and 165,977 during the first half. While that represents only about 30% of its annual objective, the company continues expanding its product strategy beyond its traditional premium intelligent EV positioning.

The launch of the MONA brand illustrates that evolution. Rather than relying exclusively on higher-priced vehicles, XPeng is targeting larger market segments where greater production volume can improve manufacturing efficiency while expanding its customer base. The recently unveiled MONA L03 represents another step in that strategy.

Li Auto delivered 30,895 vehicles in June, bringing first-half sales to approximately 193,500 units. Its family-focused SUV positioning continues to resonate with consumers, yet management is also preparing for a broader product offensive. The next-generation L6 is expected to become a major contributor during the second half, while production of updated flagship models continues to increase.

The company's longer-term objective extends beyond launching another successful model. Like several of its peers, Li Auto is attempting to reduce dependence on individual bestsellers by building a more balanced and resilient product portfolio.

Xiaomi Auto remained one of the industry's fastest-growing newcomers. Monthly deliveries stayed above 30,000 vehicles for the third consecutive month, lifting first-half deliveries to more than 169,000 units.

That performance is particularly striking because virtually all deliveries continue to come from a single model, the SU7. Few global manufacturers have achieved comparable production volume from one product so early in their automotive expansion. As Xiaomi introduces additional vehicles over the coming years, its influence within China's increasingly competitive EV market is expected to expand further.

Collectively, the first-half figures reveal an important structural change. China's startup EV market is no longer defined by numerous companies competing on relatively equal terms. Instead, it is becoming a contest where production scale, operational efficiency and technological execution increasingly determine which companies can continue investing, expanding internationally and maintaining their competitive momentum.

Three Leaders, Three Very Different Playbooks

If China's EV startups are becoming increasingly concentrated around a handful of winners, the country's established automotive groups present a more complex picture. The first-half results show that there is no single formula for success. BYD, Geely and Chery all continued expanding during the first six months of 2026, yet each is relying on a fundamentally different competitive strategy.

That diversity reflects how China's automotive industry has matured. A decade ago, leadership was largely determined by domestic sales volume. Today, investors pay equal attention to electrification, global expansion, supply-chain resilience, software capability and profitability. Scale remains important, but it is no longer sufficient on its own.

BYD Is Leveraging Scale Few Competitors Can Match

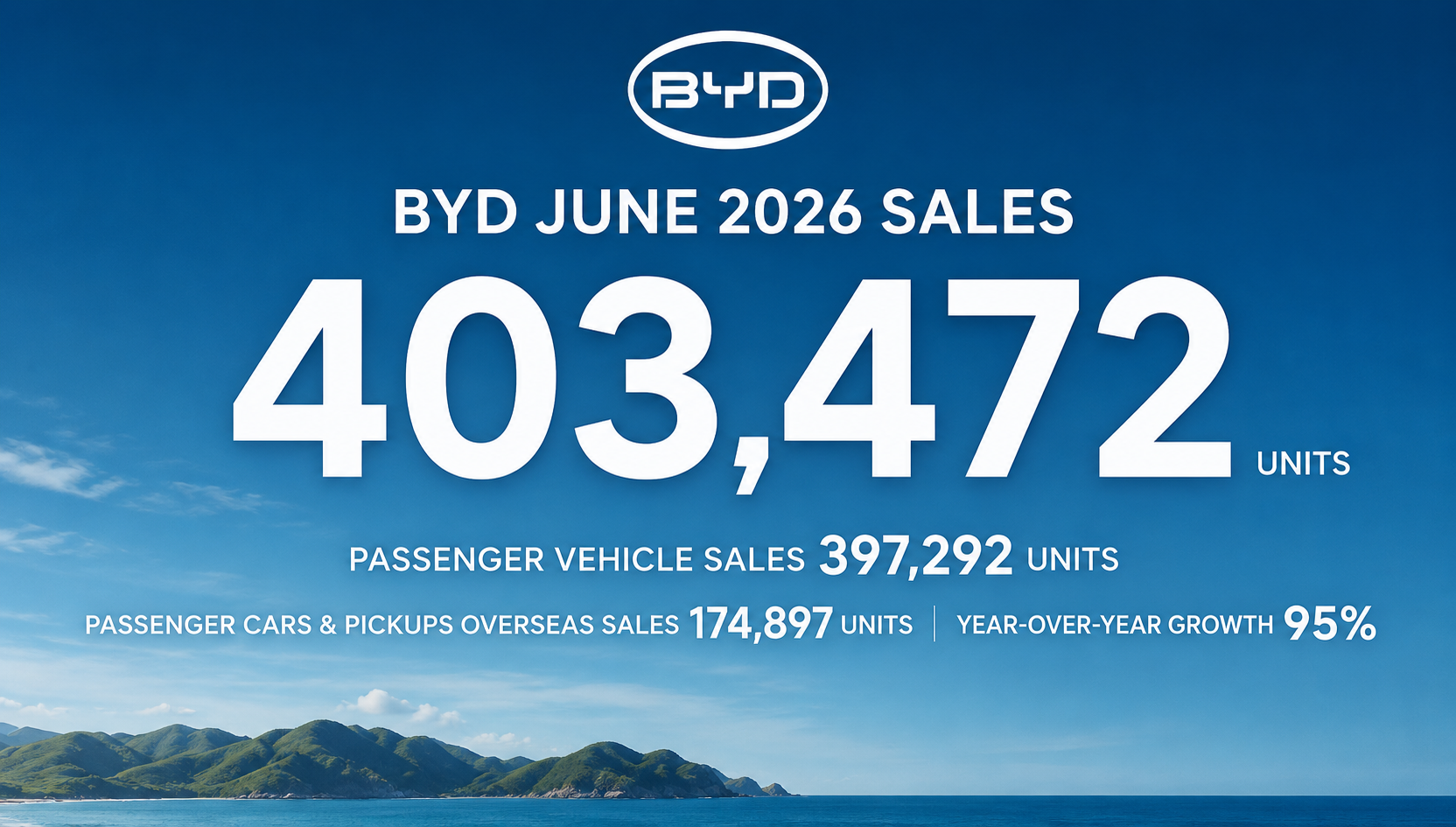

BYD once again operated in a category of its own. The company delivered 403,472 passenger vehicles in June, up 5.46% from a year earlier, pushing first-half deliveries to 1,808,511 units and reinforcing its position as the world's largest new-energy vehicle manufacturer.

Viewed in isolation, a single-digit growth rate may appear less impressive than the triple-digit expansion that characterised BYD's rise in previous years. Yet percentage growth tells only part of the story. As companies become larger, sustaining rapid expansion inevitably becomes more difficult. The more meaningful indicator is that BYD continues adding substantial volume from an already dominant base.

Delivering more than 400,000 vehicles in a single month has become an increasingly familiar achievement for the company. That consistency reflects years of investment in vertically integrated manufacturing, including batteries, semiconductors, electric powertrains and vehicle assembly. Few global automakers have built a similarly comprehensive industrial ecosystem.

The company's international business is also becoming increasingly important. Overseas deliveries continue to expand across Europe, Southeast Asia, Latin America and Australia, gradually transforming exports from a supplementary business into a meaningful pillar of long-term growth. Rather than relying solely on domestic demand, BYD is steadily evolving into a genuinely global manufacturer.

For competitors, challenging BYD is no longer simply a matter of introducing better products. Matching its manufacturing efficiency, purchasing power, cost structure and production flexibility may prove an even greater obstacle over the coming years.

Geely Is Quietly Completing One of the Industry's Most Successful Transformations

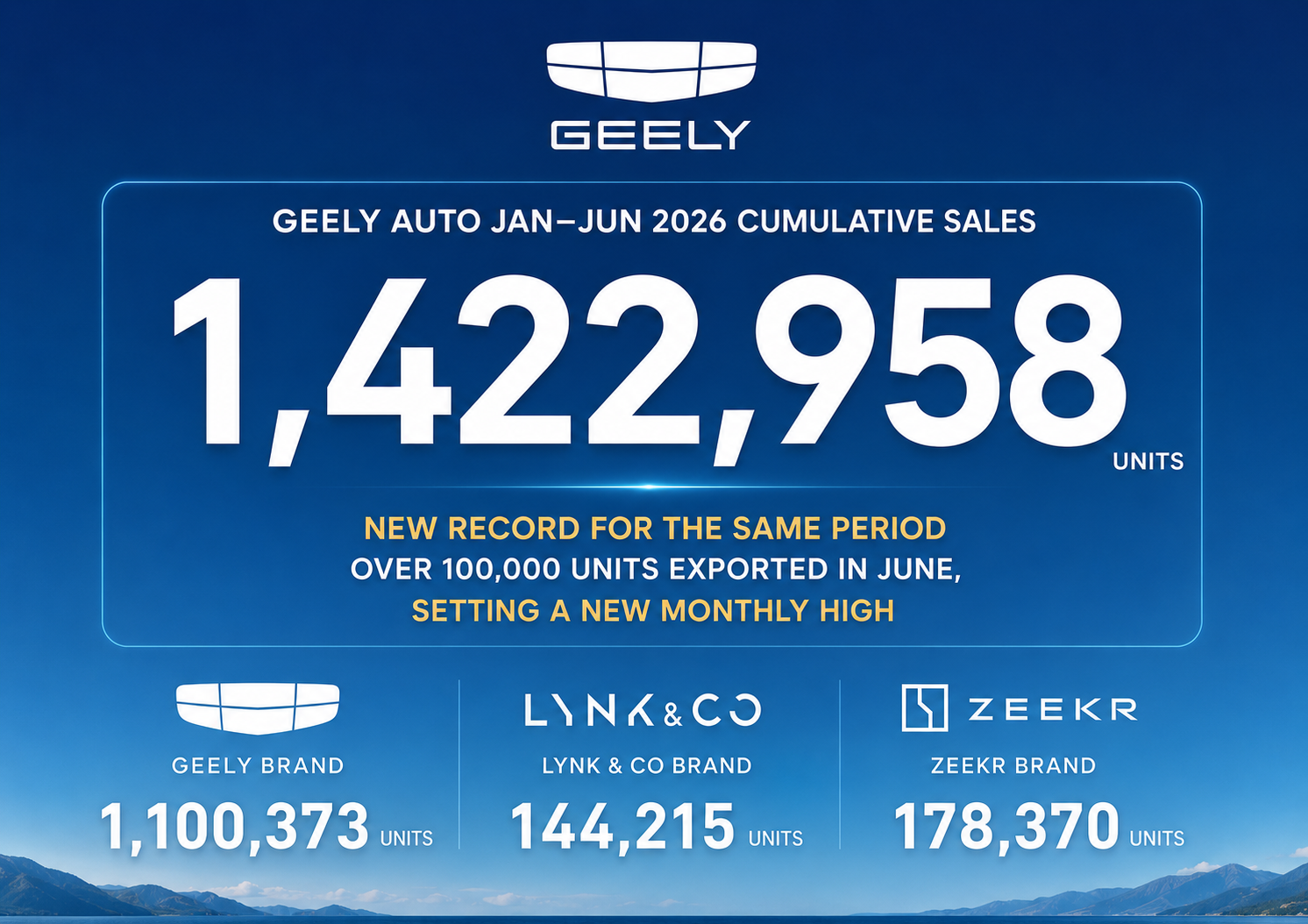

Geely's first-half performance highlights a different route to competitiveness. The group delivered 240,799 vehicles in June and 1,422,958 during the first six months of the year, both representing record performances for the period. Yet the most significant development lies beneath those headline figures.

New-energy vehicle deliveries climbed to 161,449 units in June, increasing 32% year on year and raising electrified vehicles to approximately 67% of total monthly sales. The numbers illustrate how rapidly Geely has repositioned itself from a conventional automaker into one whose future growth is increasingly driven by battery-electric and plug-in hybrid models.

International expansion has accelerated at the same time. Exports reached 102,874 vehicles in June, exceeding the 100,000-unit mark for the first time in a single month. That milestone reflects years of investment in overseas distribution networks and demonstrates that Geely's growth is becoming progressively less dependent on its home market.

The group's diversified brand portfolio also provides an advantage few rivals can match. Galaxy has become one of China's fastest-growing mainstream EV brands, while Zeekr continues strengthening its position in the premium electric segment.

Zeekr delivered 35,169 vehicles in June, more than doubling deliveries from a year earlier. First-half sales reached 178,370 units, meaning the brand has already completed nearly 60% of its published annual target—one of the highest completion rates among major Chinese EV manufacturers.

Unlike BYD, whose competitive edge is built primarily on manufacturing scale and vertical integration, Geely's strategy centres on portfolio diversification. Multiple brands, multiple market segments and multiple international regions reduce dependence on any single product cycle while creating a broader foundation for sustainable growth.

Chery Is Proving That Exports Can Be a Competitive Weapon

Chery has followed yet another path. June deliveries reached 256,612 vehicles, up 9.8% from a year earlier, while exports surged to 191,062 units, establishing another monthly record for a Chinese automaker.

Few manufacturers are as internationally oriented. More than 74% of Chery's June deliveries came from overseas markets, giving the company one of the lowest levels of dependence on domestic demand among China's major automotive groups.

That international footprint is becoming increasingly valuable. As price competition inside China remains intense, overseas markets provide additional sources of growth while reducing exposure to domestic pricing pressure. Years of investment in Latin America, the Middle East, Eastern Europe and Central Asia are now producing tangible commercial returns.

Chery's success also challenges a common assumption surrounding China's automotive industry. Although much attention has focused on battery-electric vehicles, global competitiveness increasingly depends on a broader combination of manufacturing capability, regional diversification, logistics and brand recognition. Export leadership can be just as strategically important as leadership in electrification.

Success Is Becoming More Difficult to Replicate

Despite their differing approaches, BYD, Geely and Chery share one important characteristic: each has developed a competitive advantage that extends beyond individual vehicle models.

BYD has built unmatched manufacturing scale and cost efficiency. Geely has successfully transformed itself into a diversified global mobility group with a rapidly expanding electrified portfolio. Chery has established one of China's strongest international businesses through years of overseas investment.

Those advantages are becoming increasingly difficult for competitors to imitate. As industry leaders expand production, improve profitability and strengthen cash flow, they gain additional resources to invest in research, software development, intelligent driving technologies and global expansion. Companies with weaker financial performance face the opposite dynamic, making it progressively harder to narrow the competitive gap.

The first-half figures therefore suggest that China's automotive industry is entering a new stage. Winning is no longer simply about selling more vehicles. It increasingly depends on building organisational capabilities that competitors cannot easily reproduce—a transition that may ultimately prove more significant than any single monthly sales record.

Global Carmakers Are No Longer Competing Against China — They Are Competing With China

If the first half of 2026 highlighted the growing strength of China's domestic manufacturers, it also exposed a quieter but equally significant transformation among international automakers. The companies that once defined China's passenger car market are no longer relying solely on global engineering centres or mature international platforms. Instead, they are increasingly rebuilding their competitiveness around Chinese technology, Chinese suppliers and Chinese development teams.

The shift would have been difficult to imagine only a few years ago. Foreign manufacturers traditionally viewed China as a manufacturing base and a sales market where globally developed products could be adapted for local consumers. Today, China is increasingly becoming the source of product development itself. Software, batteries, intelligent driving systems and electronic architectures are now being designed locally before influencing vehicle programmes beyond China.

Although relatively few joint-venture brands published comprehensive June delivery reports, their strategic direction has become increasingly apparent. The industry's transformation is now measured less by monthly sales figures than by where companies are investing their engineering resources and technology partnerships.

Volkswagen's partnership with XPeng is one of the clearest examples. The jointly developed China-specific electronic and electrical architecture is designed not only to shorten development cycles but also to deliver software capabilities that better match the expectations of Chinese consumers. For Volkswagen, local collaboration has evolved from a tactical decision into a central pillar of its long-term strategy in China.

Toyota has adopted a similar approach by giving its Chinese engineering organisation greater responsibility for developing future battery-electric vehicles. Nissan, through its cooperation with intelligent-driving specialist Momenta, is integrating locally developed driver-assistance technologies into upcoming models. These decisions illustrate a broader industry trend: international manufacturers increasingly recognise that competing successfully in China requires products conceived in China rather than merely adapted for it.

The implications extend well beyond individual companies. China's automotive sector has evolved from the world's largest vehicle market into one of its most influential automotive innovation ecosystems. Global manufacturers are sourcing batteries, semiconductors, software platforms and intelligent-driving technologies from Chinese partners at a pace that would have seemed unlikely only a few years ago.

This change is also reshaping the industry's development rhythm. Chinese manufacturers have normalised annual product updates, rapid software iterations and significantly shorter vehicle development cycles. International brands, once accustomed to product plans spanning four or five years, are increasingly adopting what many executives now describe simply as "China speed". The benchmark for competitiveness is no longer defined in Detroit, Wolfsburg or Tokyo alone.

Operational changes are reinforcing that technological transition. Several joint ventures have streamlined dealership networks, reduced fixed operating costs and introduced more flexible retail models. While these initiatives generate fewer headlines than new model launches, they reflect a broader effort to improve efficiency and adapt to a market where competition is increasingly defined by execution rather than legacy brand strength.

The Second Half Will Test Execution Rather Than Ambition

The first-half results suggest that China's automotive industry is no longer participating in a single competitive race. Instead, three parallel contests are unfolding simultaneously.

Among EV startups, consolidation is replacing fragmentation as scale and financial discipline become increasingly important. Established Chinese manufacturers are balancing record production with the structural transition toward electrification and global expansion. International joint ventures are rebuilding their organisations around China's technology ecosystem in an effort to regain competitiveness.

Despite these different starting points, all three groups are being measured against the same standards. Product cycles are becoming shorter. Software is now as important as hardware. Supply-chain resilience carries as much weight as manufacturing capacity. Overseas expansion is evolving from a growth opportunity into a strategic necessity.

The first half of 2026 also reinforces another powerful trend: competitive advantages are becoming increasingly self-reinforcing. Companies with greater scale generate stronger cash flow, allowing them to invest more aggressively in research, artificial intelligence, intelligent driving, battery technology and international expansion. Those falling behind face mounting pressure as declining sales restrict their ability to finance the next generation of products.

That dynamic helps explain why the gap between market leaders and the rest of the industry continues to widen. The competition is no longer determined by one successful vehicle or one strong quarter. It is increasingly defined by organisational capability, execution speed and the ability to sustain innovation across multiple product cycles.

For global investors, suppliers and policymakers, China's first-half scorecard represents far more than another monthly sales update. It offers a clear indication of where the world's largest automotive market is heading—and, increasingly, where the global automotive industry itself is likely to evolve.

The companies leading today's rankings may not remain on top simply because they are larger. Their real advantage lies in how quickly they adapt to changing technologies, consumer expectations and increasingly global competition. As the industry enters the second half of 2026, the question is no longer who can grow the fastest. It is who can evolve the fastest. Judging by the first-half results, that distinction is becoming the defining measure of success in the next era of the global automotive industry.