Nissan has spent the past two years trying to convince Chinese buyers that it can behave like a local carmaker. Its slogan has been simple enough: “in China, for China, to the world.”

Yet the Japanese group is now being pulled into a very different story — one in which Toyota, Honda, Nissan and Mitsubishi are exploring common standards for next-generation automotive technology as Japan’s legacy carmakers try to respond to the rise of Chinese rivals and Tesla.

That may be a logical industrial move. It is also a branding problem. Nissan is trying to hold two identities at once: a China-first player in the world’s most competitive electric-vehicle market, and a member of a Japanese technology bloc widely framed as a counterweight to Chinese carmakers. For consumers, the contradiction is not hard to spot.

Toyota has said talks with Nissan and Mitsubishi over next-generation vehicle technology have entered an advanced stage. Nissan chief executive Ivan Espinosa has described the discussions as “very constructive,” with chip and component standardisation among the areas under review. Japanese media have cast the wider effort around common ECU standards as a way for Japan’s carmakers to compete more effectively against Chinese companies in software-defined vehicles, as well as against Tesla.

For Nissan, the timing is uncomfortable. The company has only recently shown signs of recovering momentum in China, after years of decline for Japanese brands. A campaign built around local development, local supply chains and Chinese design preferences now risks being overshadowed by headlines suggesting that Nissan is joining an alliance to resist the very industry ecosystem it says it wants to learn from.

The Limits of a China-First Narrative

Nissan’s China strategy has not been empty rhetoric. Product authority has been pushed closer to local teams. The N7, N6 and NX8 have been led by Chinese development operations. Some newer models have adopted design details aimed more directly at Chinese buyers, including illuminated logos and more technology-led interiors. The intended message is clear: Nissan wants to be seen less as a foreign joint-venture brand and more as a locally responsive carmaker.

There is evidence that the message has started to land. Dongfeng Nissan recorded 172,800 insured vehicles in China between January and May 2026, up 6.5 per cent from a year earlier, according to the source article. That made it an unusual case among mainstream joint-venture brands: a legacy foreign player still able to show growth in a market increasingly dominated by Chinese manufacturers.

The difficulty is that brand trust depends on consistency. Nissan cannot easily reject the “countering China” framing if that is how the alliance is being publicly understood. Yet accepting it would undercut the China-focused identity it has spent two years trying to build. A company cannot ask Chinese buyers to treat it as almost local while simultaneously appearing to participate in a bloc designed to reduce dependence on Chinese technological leadership.

The investment behind this repositioning has not been trivial. Nissan’s local reset has involved roughly $1.395bn in investment and a sales base of about 100,000 units tied to its renewed China push. The risk is that a single industrial alliance, even one that makes sense on paper, can puncture a narrative that took years to construct.

Espinosa himself has acknowledged the source of the pressure. In an interview cited by the original article, he said China was becoming a benchmark for technology, cost and development speed, and that Nissan needed to learn from China before taking that know-how to other markets. That is a rational assessment. It becomes harder to defend when paired with a Japanese alliance presented as a response to China’s ascent.

This Looks Less Like an Offensive Than a Retreat

The deeper issue is not only communications. Nissan’s move toward Toyota, Honda and Mitsubishi reflects a company that has lost confidence in its ability to navigate the electric transition alone. The group’s global sales fell about 6 per cent in fiscal 2025 to roughly 3.15mn vehicles. Its Japanese domestic sales dropped 13.5 per cent to about 400,000 vehicles, the lowest level since 1993. Net losses reached ¥533.1bn, marking a second year of heavy losses.

Nissan has also been raising cash from assets. Before Espinosa took charge, the company sold its global headquarters building in Yokohama for about $628mn. It has announced plans to cut 20,000 jobs and close seven factories. When Espinosa said fiscal 2025 would be a year to restore the foundation for profitability, the subtext was blunt: survival comes before ambition.

Against that backdrop, technology cooperation with Honda and Mitsubishi looks less like a bold attack on the future than a defensive search for scale. Nissan missed the most important window in the electric transition. It now has to save cost, shorten development cycles and avoid being trapped by slower legacy systems, all at the same time.

The contradiction is visible in the timetable. Models using standardised ECUs may not reach production until 2029. Nissan, by contrast, wants to cut development cycles from 55 months to 26 months. Waiting for common Japanese standards while promising Chinese-style speed creates two opposing forces inside the same strategy.

The failed Honda merger talks expose the same problem. In December 2024, Honda and Nissan began discussions around a joint holding company. By February 2025, the talks had collapsed. Nissan’s then-chief executive Makoto Uchida later suggested that the structure had shifted toward making Nissan a Honda subsidiary — an outcome he could not accept. Nissan wants help, but not subordination. It needs partners, but cannot afford to look weak. That is a difficult position from which to rebuild competitiveness.

China’s Consumers Are Moving On

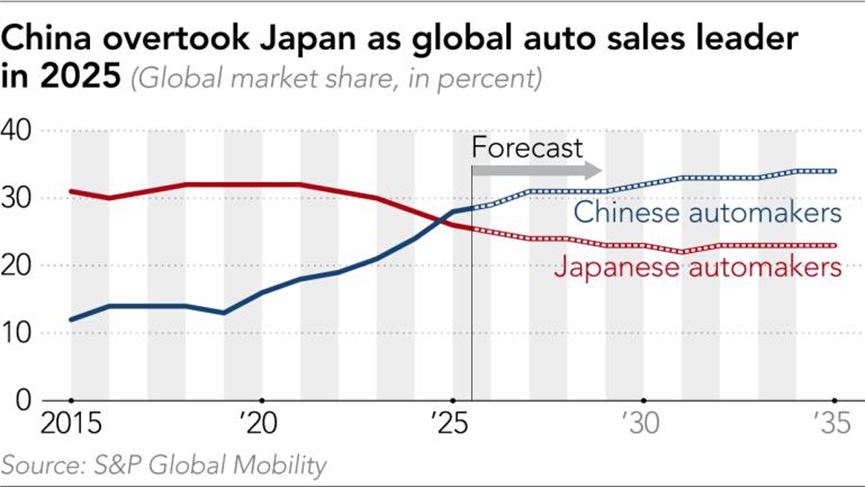

The most dangerous problem for Nissan is not a single alliance headline. It is the slow disappearance of Japanese brands from China’s consumer imagination. In 2020, Japanese marques held 23.1 per cent of the Chinese market. By 2025, that share had fallen to 9.8 per cent. In 2026, domestic Chinese brands have pushed above 70 per cent, leaving Japanese manufacturers fighting around the 10 per cent threshold.

Nissan’s own China sales have fallen from a peak of about 1.56mn vehicles to roughly 650,000. The decline is not just numerical. It reflects a generational change in buyer psychology. Japanese brands are not being actively boycotted so much as quietly removed from shopping lists. For automakers, that is more dangerous: a brand can respond to anger, but it is much harder to recover from irrelevance.

The competitive set has changed. Nissan is no longer mainly fighting Toyota or Honda in China. It is fighting BYD, Geely, Changan, Nio, Li Auto and other local players that have learned to combine battery technology, software, pricing speed and consumer-facing design in ways legacy joint ventures struggle to match.

Espinosa appears to understand the lesson. Chinese carmakers can often develop new models in about two years. Nissan has applied lessons from Dongfeng to the N7, cutting its development cycle roughly in half, and now wants to export that faster model to other markets. The direction is right. The concern is the pace. By the time Nissan masters the Chinese playbook of two years ago, Chinese competitors may already have moved on to the next one.

This is why the alliance narrative is so damaging. If the central sales pitch in China is local technology and local responsiveness, joining a Japan-led effort publicly interpreted as a counterweight to Chinese carmakers creates a direct conflict. Chinese consumers may ask a simple question: why buy a car from a company that says it is learning from China while appearing to organise against it?

Nissan’s Dilemma Is Bigger Than ECU Standards

Nissan is caught between three pressures: a China identity that now looks fragile, an electric transition it has been too slow to master, and consumers who are increasingly forgetting that Japanese brands were once default choices. No standardisation project can solve all three.

The racetrack has changed, as Espinosa has suggested. But Nissan’s answer — teaming up with other Japanese carmakers facing similar structural problems — risks looking like acceleration in the wrong direction. The company may need China’s speed, China’s suppliers and China’s engineering culture more than it needs another alliance built on the assumptions of the old global auto order.

For Nissan, the issue is not whether cooperation with Toyota, Honda or Mitsubishi is technically sensible. It may well be. The issue is whether a brand can ask Chinese consumers to believe in its local future while its global strategy appears to hedge against the rise of China’s car industry. In the world’s toughest car market, that may be too much contradiction for one company to carry.