Denza has launched the fast-charging N8L from about $47,000, filling out a product matrix that is starting to look increasingly formidable.

Introduction

For Li Hui, the executive now steering the brand’s commercial revival, the hand has become much stronger. Denza has moved from being widely written off to being viewed with cautious optimism. The question is whether it has truly evolved from relying on one successful model into a three-legged luxury strategy.

When the Denza D9 first arrived, few in the market believed the brand had much of a future. Some thought it was close to disappearing altogether. Look back a little more than three years later, and Denza has delivered one of the more unexpected turnrounds in China’s auto industry.

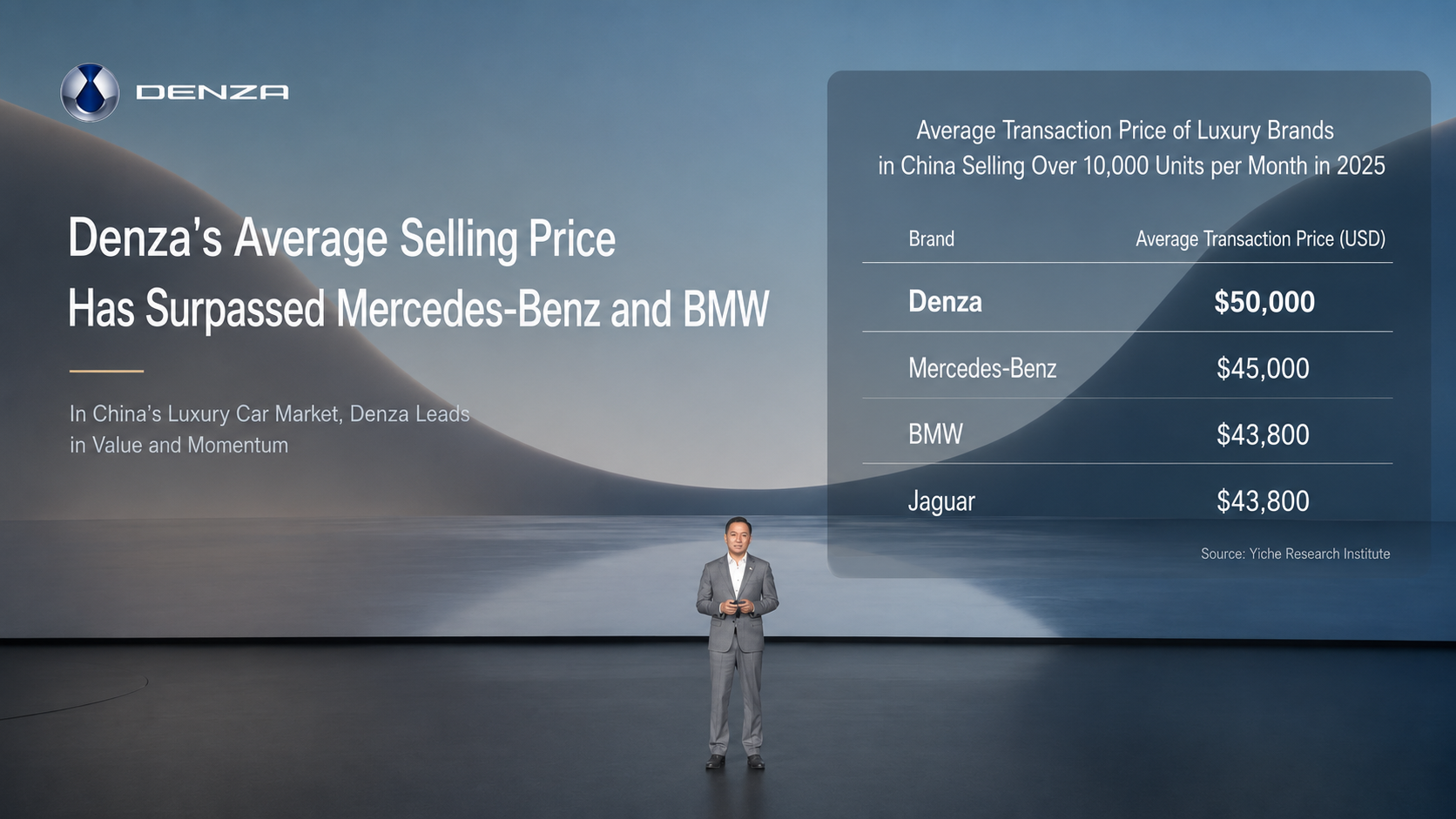

If the D9’s breakout success was the first step in winning back a ticket to the market, the figure who has helped the brand move beyond a single hit and gain a foothold in the premium segment is Li Hui, who took charge of the brand in 2025. His answer to sceptics has been performance: monthly sales above 16,000 units, an average transaction price higher than those of Germany’s traditional luxury brands, and the D9 and Z9 GT each establishing positions in their own niches. The N8L is now expected to carry another piece of that burden.

Under Li’s direction, Denza has built what looks like a three-pillar structure.

That matters because the three models cover three different segments: MPV, shooting brake-style GT and SUV. They speak to very different customers, yet they sit in a tightly defined price band of roughly $44,000 to $66,000.

Such a clear cross-category layout is hard to explain as luck.

So what is the operating logic that brought a once-dismissed brand back into the mainstream conversation?

The answer may lie in behavioural economics. It also helps explain why Denza has not leaned on a price war.

From D9 to N8L, the flywheel begins to turn

Business history has a familiar concept: the flywheel effect. The hardest part is getting the first rotation started. Once every turn adds momentum, the wheel begins to spin faster on its own.

Denza’s path fits that idea. When Li Hui took over sales, the brand had little more than a name. He did not rush to push sedans or SUVs. Instead, he went straight into the relatively open field of luxury MPVs. The timing left little room for hesitation. Buick’s GL8 was ageing, Toyota’s Alphard was expensive, and the market wanted a Chinese answer to the Alphard. Whoever filled that gap would have a chance to claim the main seat.

The D9 did exactly that. It became a hit and sold 103,460 units in 2025, retaining the annual MPV sales crown for a third consecutive year. It also ranked highly in residual value and customer satisfaction, breaking a monopoly that joint-venture brands had held for more than two decades. In hindsight, the D9 was the first rotation that got Denza’s flywheel moving.

The brand did not try to do everything at once. It concentrated resources on one category and pulled Denza from a near-death position to monthly sales of more than 10,000 units. That kind of strategic discipline is not easy to copy.

After that first turn, many argued that the D9 had simply been lucky and had ridden the MPV boom. Li then used the Z9 GT to push the flywheel through a second rotation. In May 2026, the Z9 GT sold 5,949 units in a single month, up more than 50 per cent from the previous month and marking two straight months of strong growth. It stood out in the luxury GT segment. Its customers barely overlap with those of the D9: the D9 serves business and family upgrade demand, while the Z9 GT targets individualistic luxury buyers. That suggests Denza’s product definition capability has matured.

Li once told employees: “Do not define a brand by the success of one car.”

Any carmaker chasing a multi-product strategy should sit with that sentence for a while.

The third turn of the flywheel is the newly launched fast-charging N8L.

China’s flagship family SUV market is among the fiercest battlegrounds in the country’s luxury sector. Li Auto’s L8, Aito’s M8 and Lynk & Co’s 09 are all fighting there. The N8L’s entry means Denza now uses the D9, Z9 GT and N8L as the core of a broader line-up that also includes the N9 and N7, giving it luxury coverage across MPVs, GT-style estates and SUVs. Three main models, three segments and three different customer profiles, all concentrated in the $44,000 to $66,000 range.

This is not coincidence. It is Li Hui’s flywheel strategy by design.

Once the first turn starts, every subsequent rotation stores energy for the next one. If each new model adds brand momentum rather than cannibalising the others, a wobble in any single car no longer shakes the foundation of the whole brand.

On that point alone, Denza already looks different from brands whose many products end up fighting among themselves.

Three anchors give Denza its confidence

Li Hui has made effective use of another behavioural economics idea: anchoring. Consumers do not judge whether something is expensive in absolute terms. They judge it by what they compare it with.

Li’s skill lies in using three models to drive three anchors into the market. Each one hits a point that matters to a specific set of customers. This anchoring logic has become one of Denza’s main differences from other premium Chinese brands.

The D9 anchored the idea that a luxury MPV could mean Denza. Before it arrived, the market above about $44,000 was dominated by imported or joint-venture products. Buick’s GL8 had ruled for 20 years. Toyota’s Alphard could command premiums of about $29,000 and still attract queues. The D9 used the positioning of a Chinese Alphard to fix the idea of a Chinese luxury MPV in buyers’ minds. Today, when many consumers think of a luxury MPV, the first answer is no longer necessarily the GL8 or the Alphard. It is the Denza D9.

The value of that anchor is visible in the numbers. Since launch, the D9’s retail pricing has remained relatively firm and it has avoided large-scale price wars. It sold 103,460 units in 2025, led the MPV market, and helped lift Denza’s average transaction price to about $53,000, above Mercedes-Benz and BMW. That is the answer to how much the anchor is worth.

The second anchor is the Z9 GT, which tells buyers that Denza can do luxury performance as well.

Many people assumed Denza could only make business-oriented vehicles. The Z9 GT, a shooting brake-style performance car, has broadened that perception. It anchors Denza’s technology ceiling and shows the brand is not a one-subject student. At the 2026 Beijing auto show, Li said: “China is not only capable of making cars; it can also make the world’s top supercars.” The Z9 GT’s monthly sales suggest there is a market in China for a GT priced above $44,000. The real question is whether a brand dares to build one and has the ability to make it work. Li dared, and he delivered.

The N8L is Denza’s third anchor.

Li Auto’s L8 and Aito’s M8 have already pushed this market to extremes, yet the N8L still enters because it anchors the idea of all-round luxury. For space, it offers a 5,200mm body, a 3,075mm wheelbase and a six-seat layout. For performance, it claims 0-100kph acceleration in 3.7 seconds and BYD’s Yisifang tri-motor independent-drive system. For safety, it has 2,000MPa high-strength steel in the A-pillar and a structure said to withstand the weight of a 25-tonne truck without collapse. It also brings a second-generation Blade battery, 430km of CLTC electric range, five-minute rapid charging and nine-minute full charging. By the launch date, more than 6,700 fast-charging stations had been built across China, covering almost one-third of expressway service areas. That directly addresses one of users’ biggest anxieties.

Once the three anchors are fixed, the brand’s footing becomes much firmer. A brand with that level of confidence has less to fear in competition. The D9’s pricing strength nearly four years after launch shows how deeply Li has driven those anchors into the market.

More than 60 per cent of Denza users come from traditional luxury marques such as Mercedes-Benz, BMW, Porsche and Audi. These buyers are not coming because Denza is cheap. They are coming because, in this price band, they see Denza as the better choice. Persuading owners of German luxury cars to switch voluntarily may be the strongest endorsement of the brand.

A three-legged strategy builds depth rivals will struggle to breach

Military strategists speak of strategic depth. An army cannot defend just one point. It needs buffers to the front, rear and sides so it has room to manoeuvre under attack. Denza’s three-legged approach is, in effect, an attempt to build that kind of depth at the brand level.

The D9 is the first layer of that depth and remains Denza’s base.

Business MPV customers tend to be loyal, with strong willingness to repurchase and recommend. The D9 gives Denza stable cash flow and a reputation base. The second-generation D9 further strengthens its product case and consolidates Denza’s dominance in MPVs.

The Z9 GT is the second layer. It is about brand altitude.

A shooting brake-style GT is not a mass-volume product. It is an image vehicle. Its presence tells the market that Denza is not a business-van brand but a luxury brand. The value of this layer is that it raises the ceiling for the whole marque. Li has said the Z9 GT has already been launched in several European countries and received positive feedback, helping prepare the ground for Denza’s international expansion.

The N8L is the third layer. It is about market breadth.

The family SUV is the largest single luxury segment in China. The N8L is not meant to replace the D9 or Z9 GT. It is meant to expand Denza’s user pool from business customers and style-conscious buyers to families. Once these three layers are combined, Denza’s risk resistance is no longer that of a brand that collapses if one model fails. It becomes a brand with options.

Beyond that strategic depth, Li has also built four defensive moats around Denza.

The first is supply chain control. To ensure deliveries of the fast-charging N8L, Li built up battery-pack reserves in advance and personally visited battery plants and vehicle factories to push capacity ramp-up. After the launch event, he asked production managers to implement round-the-clock three-shift operations. A company vice-president stayed at the factory for more than 10 days, leading a president-level project to prioritise N8L production quality. Many brands talk about execution. Fewer put the top executive directly on the factory floor.

The second moat is user orientation. Inside Denza, Li requires all product decisions to be validated through customer research rather than executive instinct. That decision-making mechanism is something many carmakers could learn from.

The third is technology priority. Denza enjoys preferred access to technology inside BYD. Li has said clearly that BYD’s second-generation Blade battery is being supplied to Denza first within the group. The N8L’s specification makes that clear: the second-generation Blade battery, fast-charging technology, Yisifang, DiPilot “God’s Eye” 5.0, the Yun-Nian-A intelligent air body-control system and BYD’s “Didi Xia” super-intelligent assistant are all launched first or prioritised on Denza models. That technology priority is a core reason Denza can stay competitive in the $44,000 to $66,000 range.

The final defence is channel discipline. Denza has more than 600 outlets across China, covering first-tier, new first-tier, second-tier and third-tier cities as well as some wealthy top-100 counties. Li has said the network will remain stable, with future emphasis on improving service rather than blindly adding stores. At a time when many brands are racing to expand their retail footprints, that restraint is rare. By choosing to slow down rather than build at any cost, Li may be giving Denza a longer runway.

Conclusion

Denza has used the flywheel effect to gain momentum, anchoring to win users’ confidence, and strategic depth to strengthen its resistance to risk. Its development over the past few years deserves attention. Li Hui’s strategic patience and execution have been central to that progress. His playbook is not a crude marketing push. It is a complete and repeatable operating method, and it is well suited to the current stage of Chinese brands’ move upmarket.